The Finance Bill, 2026, has proposed amendments to both the Income-tax Act, 1961 (Old Act) and the Income-tax Act, 2025 (New Act). This article will deal with the amendments pertaining to the law on reassessment.

Abstract

The Finance Bill, 2026, has proposed amendments to both the Income-tax Act, 1961 (Old Act) and the Income-tax Act, 2025 (New Act). This article will deal with the amendments pertaining to the law on reassessment.

Abstract

1. Introduction

2. Proposed amendments

2.1. Updated return after issuance of Reassessment Notice [Clause 5 and 57]

2.2. Jurisdictional Assessing Officer versus Faceless Assessing Officer [Clause 8 and 62]

2.3. Document Identification Number (DIN) [Clause 26 and 106]

3. Dénouement

xxx

1. Introduction

As mentioned in the abstract, the Finance Bill, 2026, has proposed amendments to both the Old Act and the New Act. Some of the amendments are introduced retrospectively to overcome certain High Court decisions, and some of them are introduced with the view to give the taxpayers another chance to come clean. What is clear is that the intention of the legislature is to reduce litigation. This article will critically analyse the said amendments.

2. Proposed amendments

2.1. Updated return after issuance of Reassessment Notice [Clause 5 and 57]

In the Old Act, an updated return (section 139(8A) of the Old Act) was possible only before a scrutiny notice or reassessment notice, inter alia.

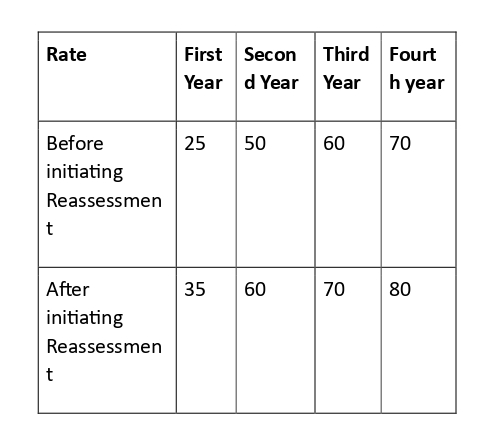

However, this is a proposed change. An amendment is proposed in section 263(3) of the New Act and section 139(8A) of the Old Act, allowing a return to be updated subsequent to a Notice of Reassessment. As per section 267 (5) of the New Act (Corresponding to section 140B of the Old Act), an updated return can be filed by paying an additional tax of 25 percent, 50 percent, 60 percent and 70 percent of the aggregate of tax and interest payable, for filing the updated return in first, second, third and fourth year, respectively from the end of the financial year succeeding the relevant tax year.

With a view to reducing litigation, it is proposed to allow updating of the return where a Reassessment Notice is issued within the stipulated period in the Notice. (Section 280 of the New Act or section 148 of the Old Act). It is further proposed that in cases where Reassessment is initiated, the additional income-tax payable shall be increased by a further sum of 10 per cent of the aggregate of tax and interest payable on account of furnishing the updated return.

A chart demonstrating the rate of tax on disclosure in the updated return is as under:

It is also clarified that this additional rate of tax will not be considered for the purpose of imposing a penalty.

This amendment will take effect from March 01, 2026, for the purpose of the Old Act.

This is a welcoming amendment with a view to reducing litigation. However, the high rate of tax raises is something that doesn’t look very attractive, especially since Vivad Se Vishwas Schemes allowed settlement of disputes without any additional tax, interest, penalty or prosecution.

2.2. Jurisdictional Assessing Officer versus Faceless Assessing Officer [Clause 8 and 62]

Section 151A of the Old Act was introduced vide Taxation and Other Laws (Relaxation and Amendment of Certain Provisions) Act, 2020, with effect from November 01, 2020.

In light of the insertion of section 151A of the Act, the CBDT Notified the E-Assessment of Income Escaping Assessment Scheme, 2022 vide Notification 18 of 2022 March 29, 2022 (2022)442 ITR 198 (St).

According to the said Notification, for the purpose of this Scheme (a) assessment, reassessment or recomputation under section 147 of the Old Act, and (b) issuance of notice under section 148 of the Old Act shall be through automated allocation in accordance with risk management strategy formulated by the Board as referred to in section 148 of the Old Act for issuance of notice, and in a faceless manner, to the extent provided in section 144B of the Old Act with reference to making an assessment or reassessment of total income or loss of assessee.

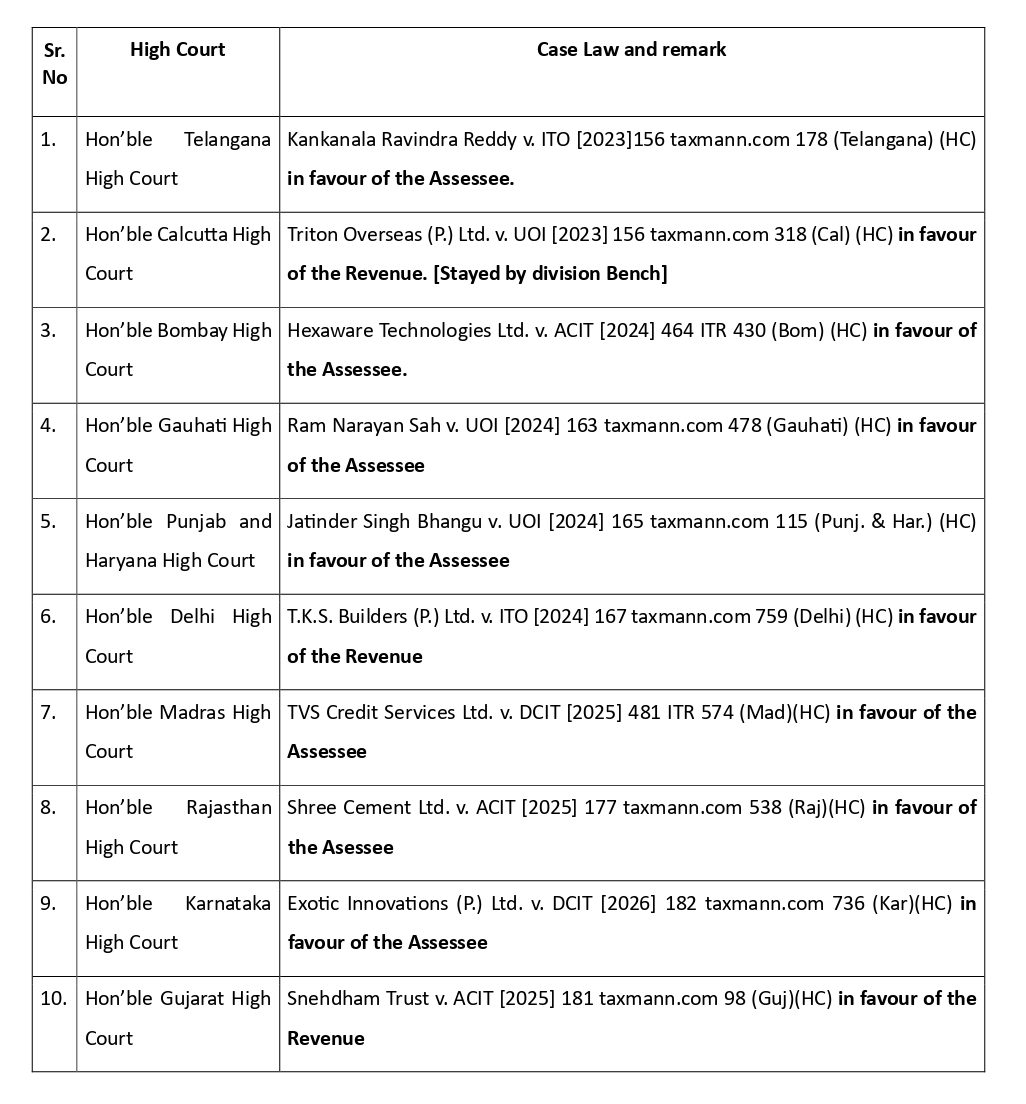

Issues cropped up regarding who is the correct authority to issue a Notice under section 148 of the Old Act.

In terms of operational order, 7 High Courts are in favour of the Assessee, and only 2 are in favour of Revenue.

The Hon’ble Supreme Court in the case of CIT v. P.J. Chemicals Ltd. [1994] 210 ITR 830 (SC) held that the conclusion reached by the majority of the High Courts cannot be said to be an unreasonable view and, on a preponderance of preferability, that view commends itself particularly in the context of a taxing statute.

An amendment is now proposed with a view to clarifying the intention of the legislature that the process followed by the Revenue is correct, and the jurisdiction to issue the Notice of reassessment lies with the Jurisdictional Assessing Officer. Further, the amendment is inserted with retrospective effect from April 01, 2021.

Pursuant to the Finance Bill, 2026, the Hon’ble Supreme Court in the case of ITO v. Vandana Malhotra SLP 57403 of 2025 dated February 03, 2026 (SC) has disposed of a petition of the revenue to file an application before the High Court in the disposed of matter to bring to the notice of the High Court the latest clarification which has been issued with effect from April 01, 2021 on such clarification to be inserted in the proposed Finance Bill. And in the event the petitioner or any other party is unsuccessful, then liberty is reserved to the aggrieved party to approach this Court to assail the impugned order as well as the subsequent order to be passed.

Now, three issues for emerging discussion: firstly, the retrospective nature of the proposed amendment, secondly, the question of legislative overreach, and lastly, the issue of time barring of reassessment.

If we remember, our former Finance Minister, Late Shri Arun Jaitley, for the same dispensation of the Central Government, had clarified in his Budget speech in 2014 (2014) 365 ITR 93(St) that the Government would not ordinarily bring retrospective amendments which could create fresh liabilities and would allow courts to come to a logical conclusion. This was reiterated in the Budget speech of 2015, (2015) 371 ITR 115(St), stating that ordinarily retrospective tax provisions adversely impact the stability and predictability of the taxation regime and resort to such provisions shall be avoided.

This spirit doesn’t seem to continue, as it is the Hon’ble Supreme Court in the case of Builders Association of India & Ors. v. UOI (1994) 207 ITR 1 (SC) held that the key legal principle is that assurances, clarifications, or opinions given by administrative authorities, or even ministers in Parliament, cannot override the statutory provisions of the law.

Secondly, whether the amendment would be considered as a legislative overreach and if this is challenged in the Court of law, would it result in another round of litigation?

Lastly, there is no stay in the orders of some High Courts, as the Notices were quashed on the first date of hearing without a stay. It can be argued that even on revival of these Notices the proceedings might be time-barred.

2.3. Document Identification Number (DIN) [Clause 26 and 106]

CBDT Circular 19 of 2019 dated August 14, 2019 (2019) 416 ITR 140 (St) mandates quoting of DIN in any Notice/Order/Summons/letter/correspondence issued by the Income-tax Department to maintain a proper audit trail. There are certain exceptions mentioned where the communication may be issued manually, but only after recording reasons in writing in the tile and with prior written approval of the Chief Commissioner/Director General of Income Tax.

It was also clarified by the Hon’ble Finance Minister Smt. Nirmala Sitharaman that a document without a DIN is invalid and should be treated as if it were never issued.

Once again, Courts took diverging views, the Hon’ble Bombay High Court in the case of Ashok Commercial Enterprises v. ACIT [2023] 154 taxmann.com 144 (Bombay)/[2023] 459 ITR 100 (Bombay) and Hexaware Technologies Ltd. v. ACIT [2024] 464 ITR 430 (Bombay) has emphasised the mandatory requirement of a document to have a DIN and the effect if it does not. A similar view was adopted in the judgment of the Madras High Court in CIT v. Sutherland Global Services Inc [2025] 175 taxmann.com 897 (Madras) and CIT v. Laserwoods US Inc [2025] 175 taxmann.com 920 (Madras), where the directions passed by the Dispute Resolution Panel without a DIN were held to be invalid. The judgments of the Delhi High Court in CIT v. Brandix Mauritius Holdings Ltd. [2023] 149 taxmann.com 238 (Delhi) as well as the Calcutta High Court in PCIT v. Tata Medical Centre Trust [2023] 154 taxmann.com 600 (Calcutta), also hold a similar view of the mandatory nature of an order to have a valid DIN.

Only the Hon’ble Jharkhand High Court in the case of Prakash Lal Khandelwal v. CIT [2023] 151 taxmann.com 72 (Jharkhand) has taken a diverging stand.

The Finance Bill 2026, proposes to amend section 292B of the Old Act and the corresponding section in the New Act to clarify that, no assessment in pursuance of any of the provisions of Old Act shall be invalid or shall be deemed to have been invalid on the ground of any mistake, defect or omission in respect of quoting of a computer generated DIN, if such assessment order are referenced by such number in any manner. Further, this amendment seeks to clarify that as long as there is a reference to DIN in the assessment order, the same would be sufficient compliance even if there may be some minor mistakes, defects or omissions in notices or summons in relation to such assessment.

The Amendment is proposed to have a retrospective effect from October 01, 2019.

In addition to the same issues raised for section 151A of the Old Act, a new issue that comes to notice is that the amendment only talks about the assessment and assessment order and does not refer to statutory notices, sanctions, and other communications.

If a view is taken that the amendment is only for the assessment order, it would further strengthen the case where Reassessment Notices, Sanction and approvals are without a valid DIN. Further, the failure to issue notices and orders with DIN number is due to in efficiency of the tax authorities. Without making such authorities responsible, the assesses are being punished by these retrospective amendments.

3. Dénouement

From analysing the proposed amendments, it is clear that the intention of the legislature is to reduce litigation in the sphere of reassessment. A similar claim was made by the Hon’ble Finance Minister while introducing the Finance Bill, 2021, that the assessments will reach finality in three years, as the assessments can be reopened till 3 years only three years from the end of the relevant assessment year, subject to certain conditions. But the subsequent amendments have, for all practical purposes, expanded the scope of the period of reopening to ten years. Thus, the purpose of the amendment in the year 2021 was defeated. However, the manner of bringing in the amendments and the effectiveness of these new policies are questionable. As it hardly enhance the Government’s push for ease of doing business in India. The direct tax regime is still as uncertain as it was prior to May 2014, if not more.

[Source : AIFTP Journal February 2026 Volume 28 No. 11]

About the Author: Details are awaited

Pdf file of article: Click here to Download

Posted on: March 18th, 2026

Leave a Reply