Prosecution Provisions – Income Tax Act, 1961 and Income Tax Act, 2025

I Existing Provisions and Proposed Amendment.

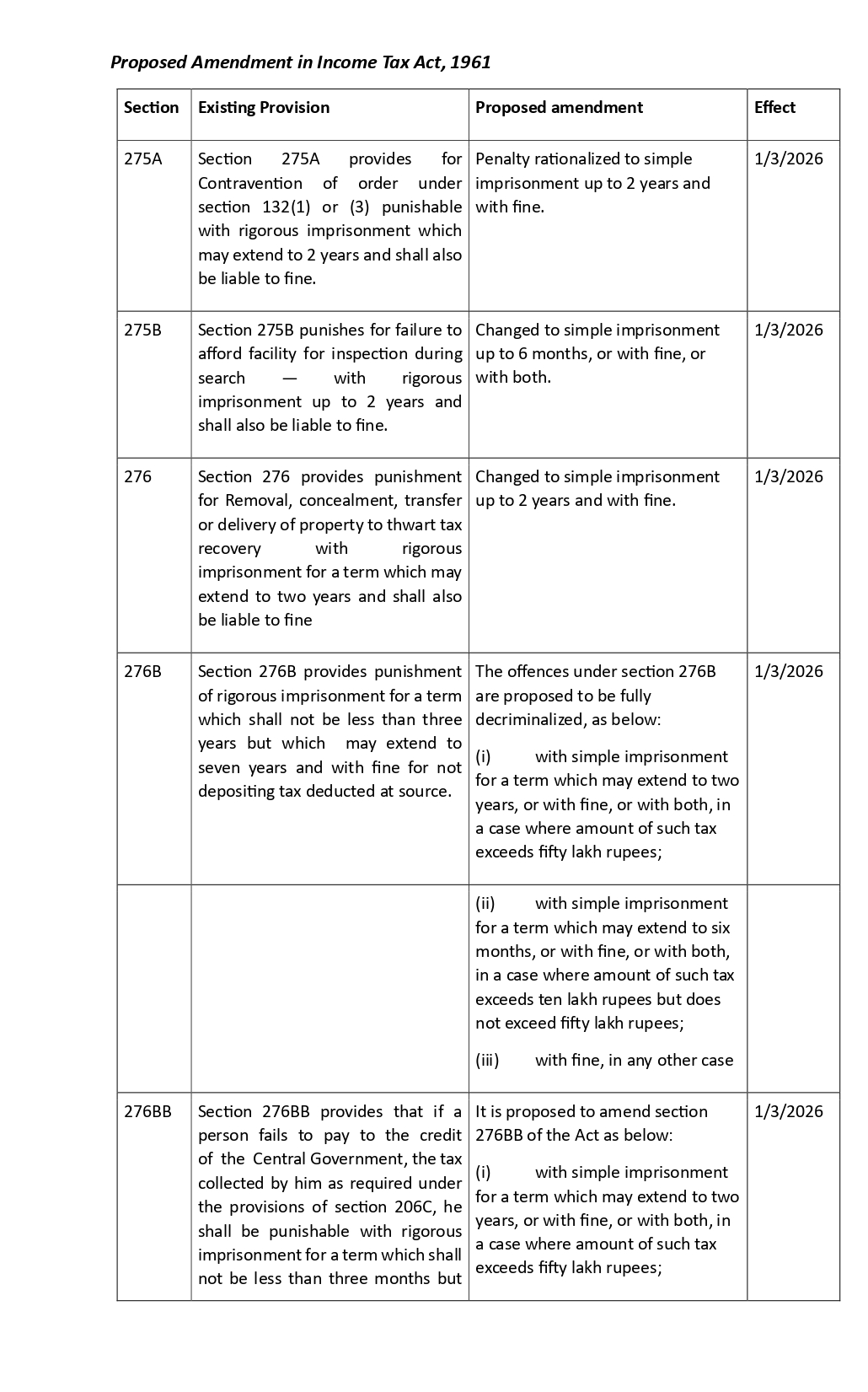

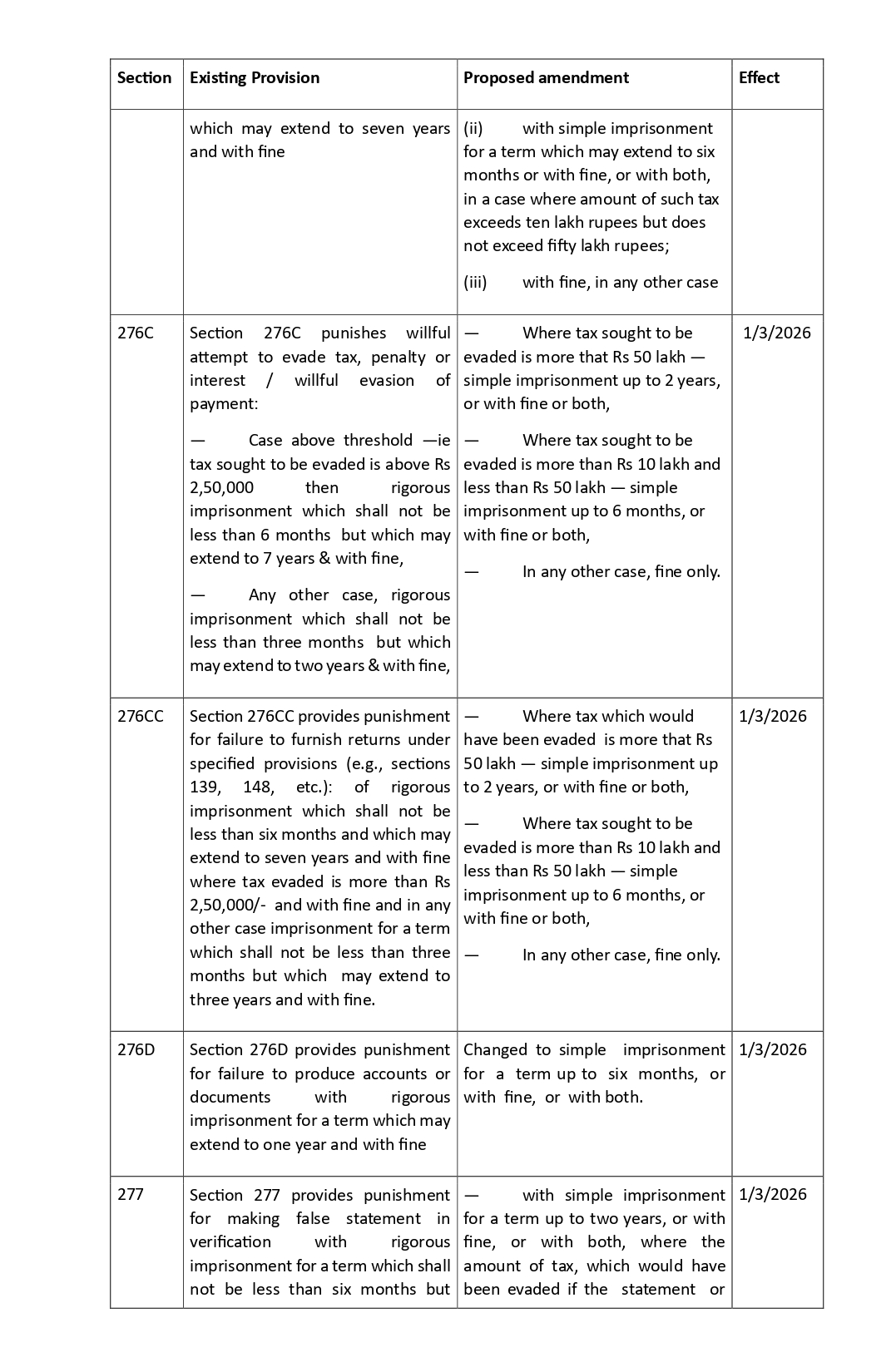

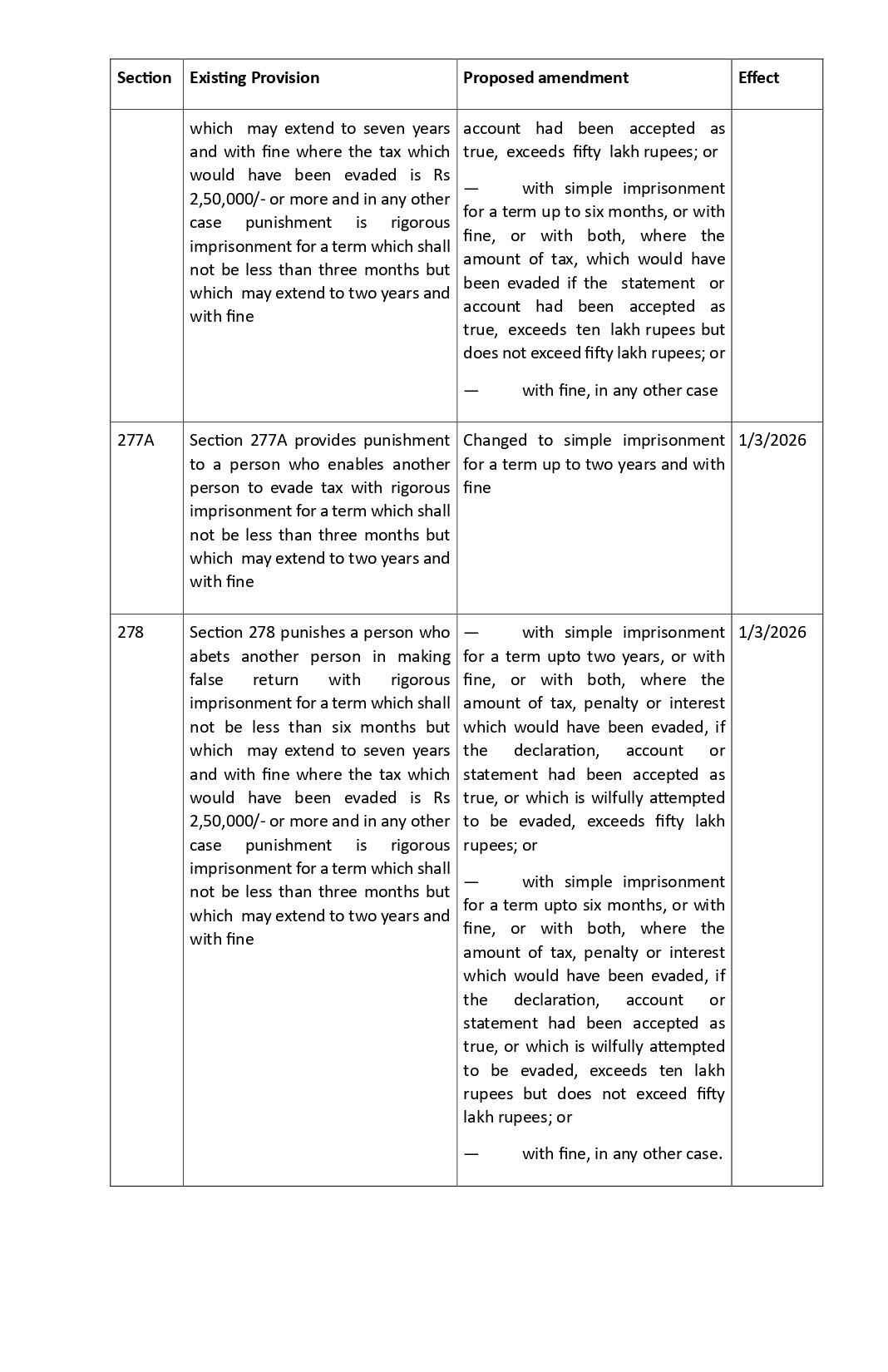

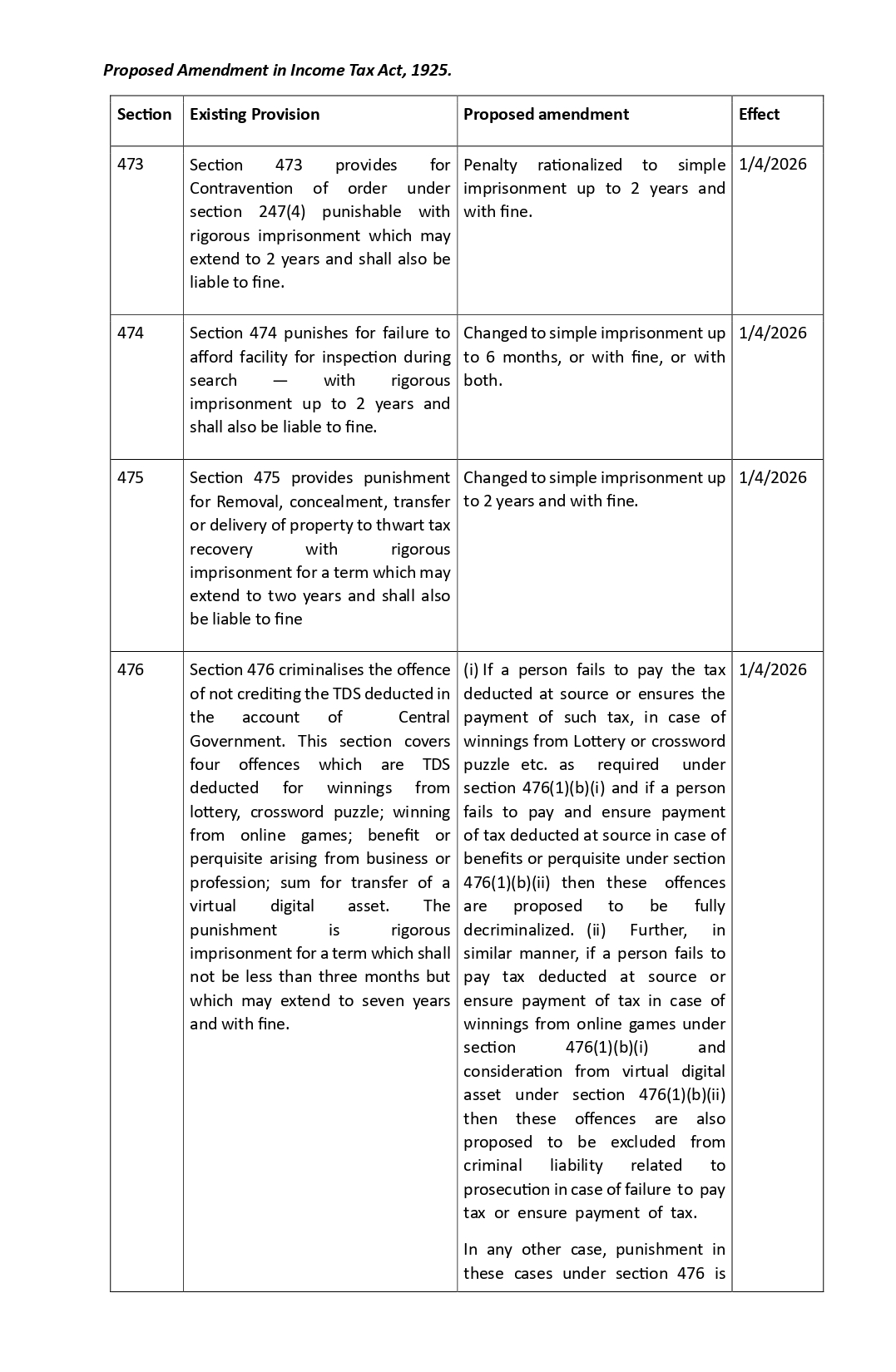

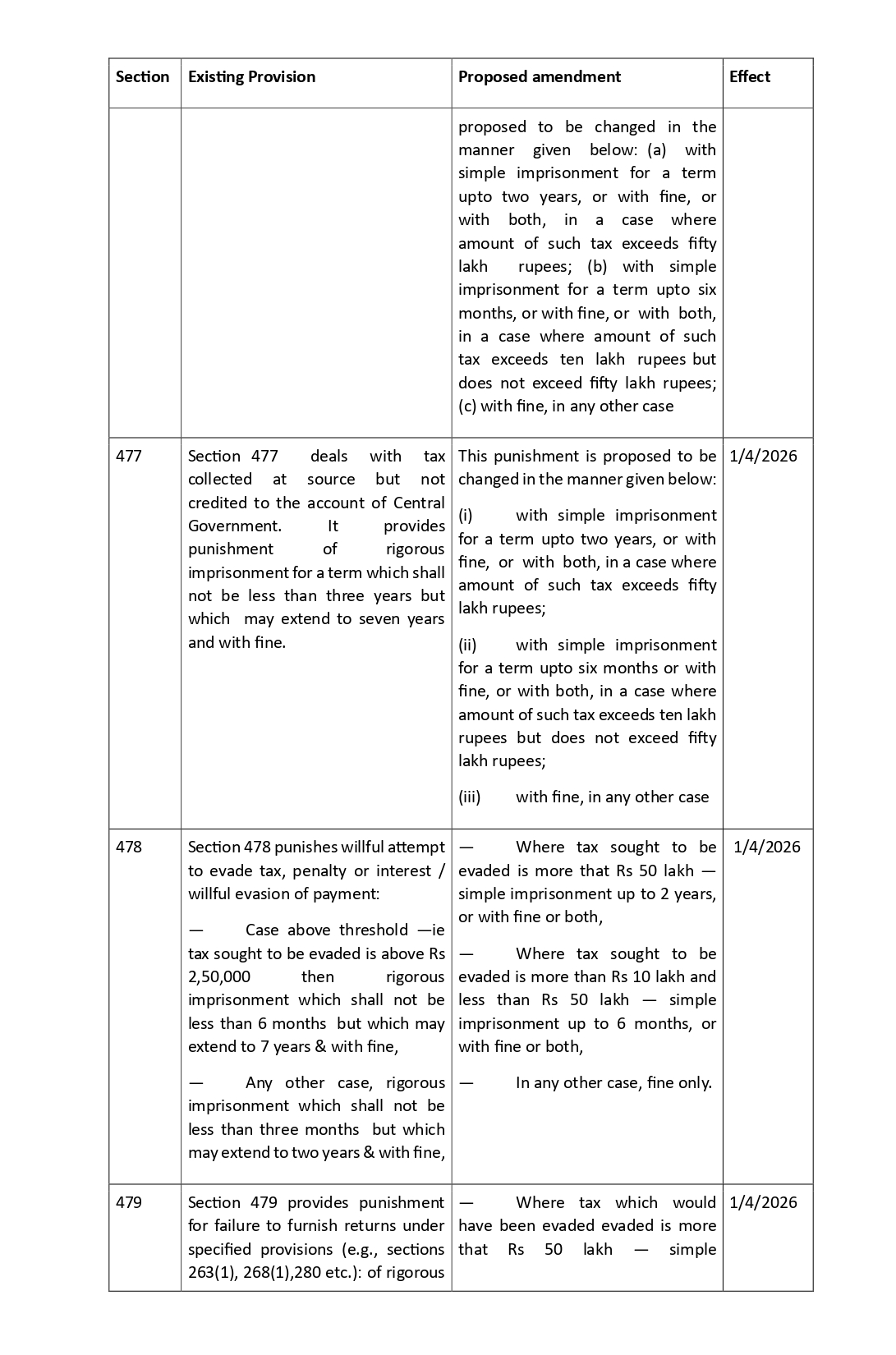

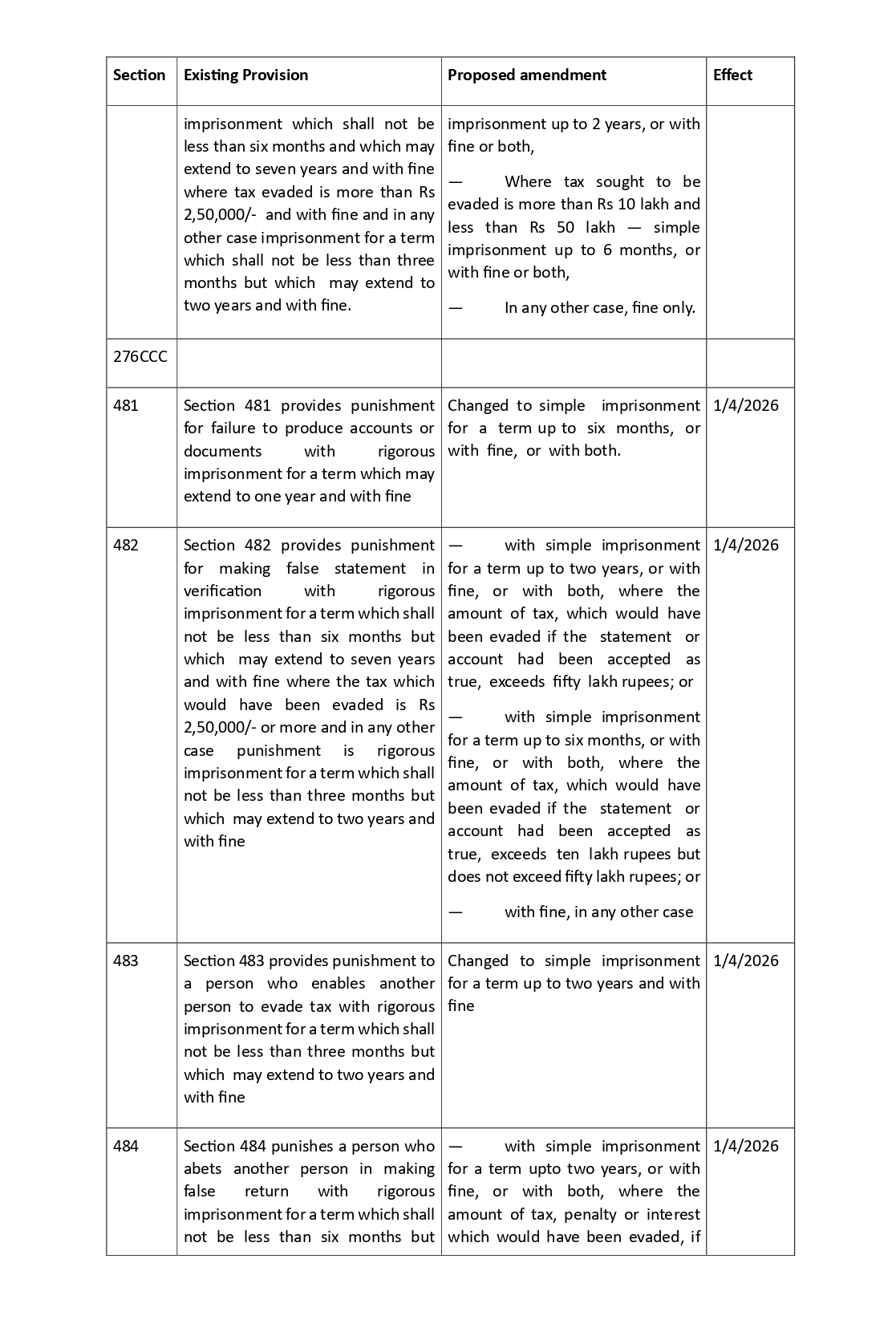

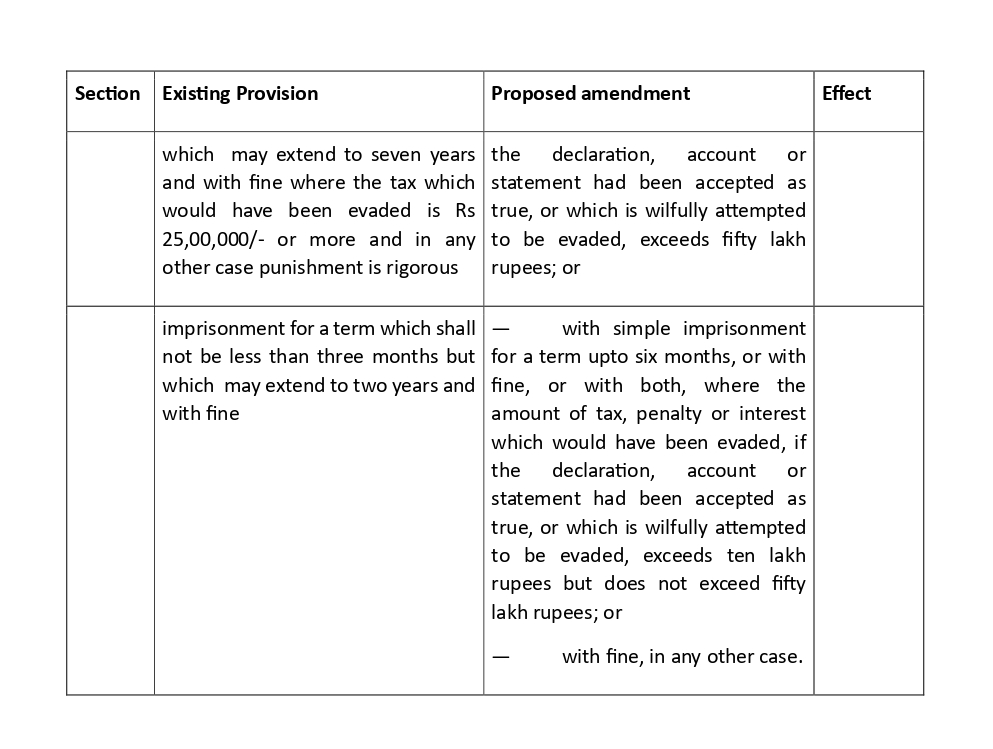

The existing prosecution proceedings and the proposed amendments in the Income Tax Act, 1961 and Income Tax Act, 2025 are as under :

II Reason for Amendments

Income-tax Act, 2025/Income Tax Act, 1961 has various provisions which imposes criminal liability on assessee and prescribes imprisonment including rigorous imprisonment which span from three months to seven years for various offences including falsification of books of accounts, failure to credit TDS/TCS deducted, tendering false statement, wilful attempt to evade tax, failure to furnish return within due time, abatement of false return, removal/concealment/transfer of property to evade recovery of tax, failure to follow certain directions of AO, etc.

In this regard, the Finance Bill, 2026 has proposed to amend provisions dealing with prosecution in light of continued exercise of decriminalisation and to make the punishment for the offences proportionate to the crimes.

The principles that are followed in the proposed decriminalization exercise are as follows:

(a) The nature of punishment is changed from rigorous imprisonment to simple imprisonment wherever prescribed in the sections mentioned above.

(b) Maximum punishment is proposed to be limited to 2 years from its current 7 year and for the subsequent offences, it is reduced to 3 years from its current 7 years.

(c) Wherever punishment of offences is prescribed based on certain grading of amount of tax evaded, new grading of offences and its corresponding punishment is prescribed.

(d) For amount of tax evaded does not exceeds ten lakh rupees, punishment of only fine is prescribed.

(e) Imposition of fine is introduced in lieu of or in addition of imprisonment.

(f) Certain offences are fully decriminalized

ANALYSIS

Substituted and deemed to be Substituted

The amendments in the Income-tax Act, 1961 are stated to come into force with effect from 1/3/2026. The Finance Bill, 2026 specifically provides that the amended provisions are “substituted and deemed to be substituted”.

The expression “substituted” ordinarily implies that the earlier provision is repealed and replaced by the new provision as if it stood in that form from the effective date. The use of the further deeming fiction “deemed to be substituted” clearly indicates legislative intent to give the amendment retrospective operation from 1/3/2026.

Thus, even if the Finance Bill, 2026 becomes an Act after 1/3/2026, the amended prosecution provisions will operate with effect from 1/3/2026 and will govern all proceedings from that date onwards.

Shall also be liable to fine

Under the pre-amended provisions of the 1961 Act and the 2025 Act, various offences were punishable with imprisonment and the language used was “shall also be liable to fine”. This formulation mandated imprisonment while giving discretion to the Magistrate to impose fine in addition to imprisonment.

The proposed amendment substitutes the words “shall also be liable to fine” with the expression “with fine”. The effect of this substitution is that fine now forms part of the prescribed punishment framework itself rather than being an additional discretionary consequence.

The sentencing structure is therefore rationalised and aligned with the graded punishment system introduced under the Finance Bill, 2026.

Cognisable v/s non-cognisable

As per the Bharatiya Nagarik Suraksha Sanhita, 2023, offences under laws other than the Bharatiya Nyaya Sanhita, 2023 which are punishable with imprisonment of less than three years are non-cognisable and bailable, unless specifically provided otherwise.

Under Section 279A of the Income-tax Act, 1961 and Section 492 of the Income-tax Act, 2025, certain offences punishable with more than three years were declared to be non-cognisable. However, ambiguity existed regarding their bailable nature. Further, offence under Section 276B (failure to deposit TDS) was not covered under Section 279A and was therefore treated as cognisable.

Now, pursuant to the proposed amendments, since the maximum punishment for all offences is reduced to below three years (generally up to two years and up to three years for subsequent offences), all such offences fall within the category of offences punishable with less than three years.

Consequently, all such offences become non-cognisable and bailable.

Summons Case v/s Warrant Case

As per Section 280C of the Income-tax Act, 1961 and Section 497 of the Income-tax Act, 2025, offences punishable with imprisonment up to two years or with fine or with both are deemed to be summons cases.

In summons triable cases:

— There is no provision for framing of charge.

— No discharge application is maintainable.

— Procedure is comparatively summary in nature.

Since under the proposed amendments the maximum punishment for most offences is capped at two years, such offences would be treated as summons cases.

Thus, all prosecution proceedings under these provisions would now be governed by the simplified procedure applicable to summons cases.

Whether lesser punishment is applicable to ongoing cases

The Supreme Court in the case of T. Barai v. Henry Ah Hoe (1983) 1 SCC 177 has held that beneficial amendments to the law could be applied retroactively to ongoing court cases, even if the amendment was not in place when the offence had occurred. In A.K. Sarkar vs. State of West Bengal MANU/SC/0181/2024 accused was punished under the Prevention of Food Adulteration Act, 1954 with six months imprisonment but as said Act was repealed and replaced by the Food Safety and Standards Act, 2006 wherein a punishment was only fine, it was held that the benefit from such lighter punishment was available to the accused.

CONCLUSION

The Finance Bill, 2026 represents a structural shift in tax criminal jurisprudence as under:

— Rigorous imprisonment eliminated.

— Maximum punishment drastically reduced.

— Fine-only regime for minor tax exposure.

— All offences become non-cognisable and bailable.

— All offences become summons triable.

— Beneficial amendments apply to pending cases.

The cumulative effect is a clear movement toward decriminalisation, proportionality, and procedural softening of tax offences.

[Source : AIFTP Journal February 2026 Volume 28 No. 11]

About the Author: Details are awaited

Pdf file of article: Click here to Download

Posted on: March 18th, 2026

Leave a Reply