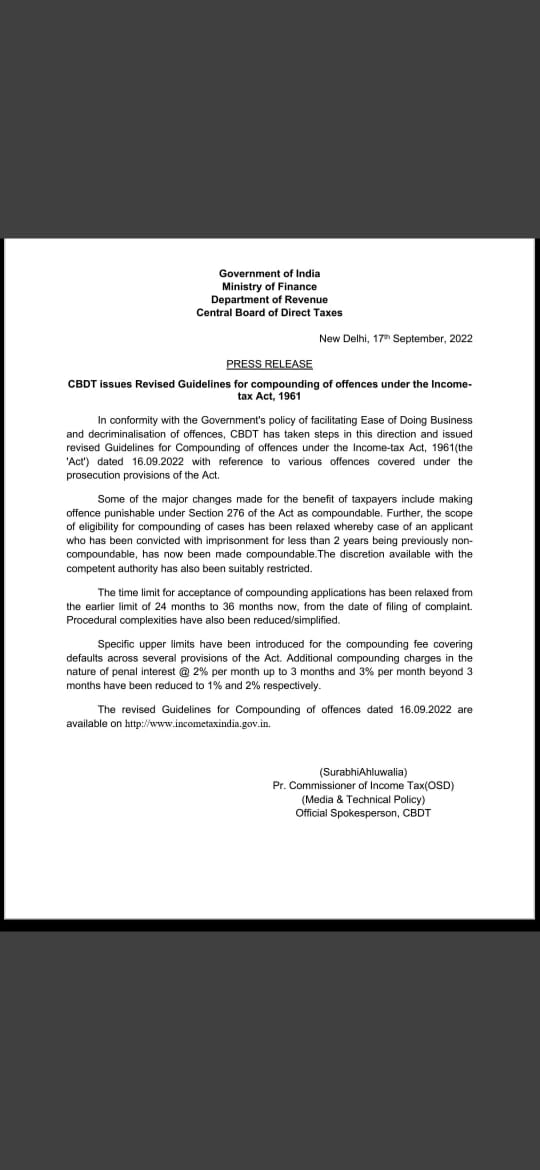

Government of India Ministry of Finance

Department of Revenue Central Board of Direct Taxes

New Delhi, 17 September, 2022

PRESS RELEASE

CBDT issues Revised Guidelines for compounding of offences under the Income tax Act, 1961

In conformity with the Government’s policy of facilitating Ease of Doing Business and decriminalisation of offences, CBDT has taken steps in this direction and issued revised Guidelines for Compounding of offences under the Income-tax Act, 1961(the ‘Act’) dated 16.09.2022 with reference to various offences covered under the prosecution provisions of the Act.

Some of the major changes made for the benefit of taxpayers include making offence punishable under Section 276 of the Act as compoundable. Further, the scope of eligibility for compounding of cases has been relaxed whereby case of an applicant who has been convicted with imprisonment for less than 2 years being previously non compoundable, has now been made compoundable. The discretion available with the competent authority has also been suitably restricted.

The time limit for acceptance of compounding applications has been relaxed from the earlier limit of 24 months to 36 months now, from the date of filing of complaint. Procedural complexities have also been reduced/simplified.

Specific upper limits have been introduced for the compounding fee covering defaults across several provisions of the Act. Additional compounding charges in the nature of penal interest @ 2% per month up to 3 months and 3% per month beyond 3 months have been reduced to 1% and 2% respectively.

The revised Guidelines for Compounding of offences dated 16.09.2022 are available on http://www.incometaxindia.gov.in.

(Surabhi Ahluwalia)

Pr. Commissioner of Income Tax(OSD)

(Media & Technical Policy)

Official Spokesperson, CBDT

Government of India Ministry of Finance

Department of Revenue Central Board of Direct Taxes

New Delhi, 17 September, 2022

PRESS RELEASE

CBDT issues Revised Guidelines for compounding of offences under the Income tax Act, 1961

In conformity with the Government’s policy of facilitating Ease of Doing Business and decriminalisation of offences, CBDT has taken steps in this direction and issued revised Guidelines for Compounding of offences under the Income-tax Act, 1961(the ‘Act’) dated 16.09.2022 with reference to various offences covered under the prosecution provisions of the Act.

Some of the major changes made for the benefit of taxpayers include making offence punishable under Section 276 of the Act as compoundable. Further, the scope of eligibility for compounding of cases has been relaxed whereby case of an applicant who has been convicted with imprisonment for less than 2 years being previously non compoundable, has now been made compoundable. The discretion available with the competent authority has also been suitably restricted.

The time limit for acceptance of compounding applications has been relaxed from the earlier limit of 24 months to 36 months now, from the date of filing of complaint. Procedural complexities have also been reduced/simplified.

Specific upper limits have been introduced for the compounding fee covering defaults across several provisions of the Act. Additional compounding charges in the nature of penal interest @ 2% per month up to 3 months and 3% per month beyond 3 months have been reduced to 1% and 2% respectively.

The revised Guidelines for Compounding of offences dated 16.09.2022 are available on http://www.incometaxindia.gov.in.

(SurabhiAhluwalia)

Pr. Commissioner of Income Tax(OSD)

(Media & Technical Policy)

Official Spokesperson, CBDT

About the Author: CA Milind Wadhwani B.COM(Hons.), DISA(ICAI), FAFD(Cert.), CCCA(Cert.), Research (Ph.D.) Scholar Mobile +91 9826273333 Mail ID: - MILIND.WADHWANI20@GMAIL.COM

Pdf file of article: Click here to Download

{kind=link}

Posted on: September 18th, 2022

A listing of which offences have been added for compounding earlier not there would help