Law on the existing provisions of reopening is to a great extent settled. However with the introduction of completely new provisions, lot of uncertainty is now created amongst tax payers as well as tax administrators. Even Courts are finding it difficult to learn and interpret these new provisions. In this paper, we plan to discuss the new provisions threadbare and analyse the issues likely to arise in implementing and interpreting the same in times to come.

CONTENTS

|

1. |

Introduction |

|

2. |

Section 147: Income escaping assessment. · Omission of the phrase ‘reason to believe’. · Validity of other items of addition in a reassessment without adding the very item which was the ground for reopening. · Principles of Merger after deletion of 3rd proviso to old S.147. · Effect of deletion of Explanation 2 – Deemed Escapement |

|

3. |

Section 148: Issue of notice where income has escaped assessment. · Meaning of ‘Information’ which ‘suggests’ escapement of income chargeable to tax. · When AO shall be ‘Deemed’ to have Information which suggests escapement of income chargeable to tax. · Period of reopening – in the cases of Search & Survey. · Inter-play between S. 147 and S. 148. · Deemed Escapement vs Information which suggests that the income chargeable to tax has escaped assessment. |

|

4. |

Section 148A: Conducting inquiry, providing opportunity before issue of notice under section 148. · Procedure under clauses (a) to (d) of section 148A of the Act. · Notice under clause (b) needs to be served properly. · Exception to procedure prescribed u/s 148A. · Challenge to order u/s 148A(d) read with notice u/s 148 of the Act. |

|

5. |

Section 148B: Prior approval for assessment, reassessment or re-computation in certain cases. |

|

6. |

Section 149: Time limit for notice. · Reopening beyond 3 years – various conditions · Asset criteria. · Is reopening permissible for escaped income not represented in the form of asset, expenditure or entry? · Years where limitation has expired under the old regime cannot be reopened under the new extended time limit · Search related cases – only ‘asset’ criteria for reopening beyond 6 years |

|

7. |

Section 151: Sanction for issue of notice. |

|

8. |

Section 151A: Faceless assessment of income escaping assessment. |

|

9. |

Other legal arguments · Escapement of Income · Change of Opinion · Reopening not permissible for roving and/or fishing inquiries · Live nexus- Cause and Effect relationship between reasons and income escaping assessment |

|

10. |

Reopening under the old regime even after new regime has come into force · Table explaining limitation for various years |

|

11. |

Conclusion |

1. Introduction

1.1. Under the Scheme of the Income Tax Act, 1961 (‘the Act’ for short), there are various remedial measures viz. reopening, rectification and revision for taking appropriate actions to plug revenue leakages when they come to notice. Reopening is perhaps the most preferred remedial measure.

1.2. The law governing reopening has more or less remained the same since 1961. Prior to 1989 there were 3 distinct conditions which were required to be fulfilled before the assessing officer (AO for short) could exercise jurisdiction to reopen viz.

(i) AO must have reason to believe that income has escaped assessment;

(ii) AO must have reason to believe that such escapement is a result of failure on the part of the Assessee to make a return or to disclose fully and truly all material facts necessary for his assessment for the relevant year;

(iii) Reason to believe should be in consequence of information received after the original assessment.

With effect from 1989, the law has once again undergone a major change. However, the spirit and substance of the provisions were retained in as much as instead of clauses (a) and (b), entire provision was enacted as one. Under the amended provision, if the assessing officer has reason to believe that any income chargeable to tax has escaped assessment he could exercise the powers of reopening. Concept of information was discarded. Proviso was added to the main section so as to provide for further safe guard to the assessees whose assessments were framed under section 143(3) of the Act. Such assessment were allowed to be reopened beyond the prescribed period of four years from the end of the relevant assessment year if and only if an income chargeable to tax has escaped assessment by reason of failure on the part of the assessee–

(i) to make a return under section 139 or in response to the notice issued under sub-section (1) of section 142 or section 148;

OR

(ii) to disclose fully and truly all material facts necessary for his assessment for that Assessment Year

1.3. Now, with effect from 01/04/2021, the law governing the provisions of reopening has been completely overhauled. The system of writing reasons of reopening before initiating the proceedings has been done away with. Inquiries and proceedings prior to issuance of notice u/s 148 have been introduced. “Reason to believe” is omitted. Search cases are covered under the provisions of reopening. Time limit to reopen is modified in a major way and for cases involving income escaping assessments amounts to or likely to amount to Rs 50 lakh and above, are extended up to 10 years. Additional protection in the cases of scrutiny assessment not allowed to be reopened beyond a period of 4 years from the end of the relevant assessment year unless there is failure in disclosing fully and truly all material facts necessary is now taken away. Information that could trigger reopening is defined. These provisions were further modified by Finance Act, 2022 so as to expand its scope, take care of some anomalies and iron out some interpretational issues.

1.4. Law on the existing provisions of reopening is to a great extent settled. However with the introduction of completely new provisions, lot of uncertainty is now created amongst tax payers as well as tax administrators. Even Courts are finding it difficult to learn and interpret these new provisions. In this paper, we plan to discuss the new provisions threadbare and analyse the issues likely to arise in implementing and interpreting the same in times to come.

2. Section 147: Income escaping assessment.

If any income chargeable to tax, in the case of an assessee, has escaped assessment for any assessment year, the Assessing Officer may, subject to the provisions of sections 148 to 153, assess or reassess such income or recompute the loss or the depreciation allowance or any other allowance or deduction for such assessment year (hereafter in this section and in sections 148 to 153 referred to as the relevant assessment year).

Explanation.—For the purpose of assessment or reassessment or recomputation under this section, the Assessing Officer may assess or reassess the income in respect of any issue, which has escaped assessment, and such issue comes to his notice subsequently in the course of the proceedings under this section, irrespective of the fact that the provisions of section 148A have not been complied with.

Omission of the phrase ‘reason to believe’.

2.1. If one compares old S. 147 with the new one, it will be noticed that under the old section the opening words were “If the Assessing Officer has reason to believe that any income chargeable to tax has escaped assessment for any assessment year”. As against the same now the opening words are: “If any income chargeable to tax, in the case of an assessee, has escaped assessment for any assessment year”. So what is missing from the section is the term “reason to believe”.

In other words, under the new provisions, S. 147 of the Act can be invoked only if any income chargeable to tax has “escaped assessment”. At this stage, I would like to invite a striking difference between the erstwhile provisions of section 147 of the Act and the present provisions of section 147 of the Act. The said difference is as follows:

· Up to 31.03.21 – Section 147 could have been invoked if the Assessing Officer has “reason to believe” that any income chargeable to tax has “escaped assessment” for any assessment year;

· W.e.f. 01.04.21 – Section 147 can be invoked if any income chargeable to tax has escaped assessment.

Perusal of the above would indicate that the concept of “reason to believe” has been given a complete go-bye and the entire emphasis for invoking section 147 of the Act is on “escapement of income”. Thus, as per the existing provisions, an Assessing Officer has to prove beyond any shadow of doubt that there is “escapement of income”. Unless “escapement of income chargeable to tax” is proved, provisions of section 147 of the Act cannot be invoked.

Therefore it is all the more important to understand the meaning of the phrase ‘reason to believe’. In the case of Desai Bros. (240 ITR 121) the phrase ‘reason to believe’ has been explained by Hon’ble Gujarat High Court with reference to a decision of the Apex Court in the case of Barium Chemicals Ltd. v. Company Law Board AIR 1967 SC 295, whereby it is stated thus:

"Undoubtedly, the word ‘reason to believe’ relates to process of entertaining an opinion which is subjective in nature and is not liable to be scrutinised by the objective test of judicial scrutiny as in appeal. However, even in the case where an action is founded on subjective satisfaction, the process of entertaining such belief is not bereft of any minimum safeguard against arbitrariness.

The limitation of judicial review where the act is to be founded on subjective opinion on the part of the authority has been succinctly stated by the Apex Court in Barium Chemicals Ltd. v. Company Law Board [1966] 36 Comp. Cas. 639. The court did not approve the unbridled and unguided operation of the freedom from judicial scrutiny of acts which are founded on formation of subjective satisfaction of the authority empowered to take such action. Shelat, J. in his opinion stated (pages 688-89) :

‘The words, ‘reason to believe’ or ‘in the opinion of’ do not always lead to the construction that the process of entertaining ‘reason to believe’ or ‘the opinion’ is an altogether subjective process not lending itself even to a limited scrutiny by the court that such ‘a reason to believe’ or ‘opinion’ was not formed on relevant facts or within the limits or . . . restraints of the statute as an alternative safeguard to rules of natural justice where the function is administrative . . .

It is hard to contemplate that the Legislature could have left to the subjective process both the formation of opinion and also the existence of circumstances on which it is to be founded. It is also not reasonable to say that the clause permitted the authority to say that it has formed the opinion on circumstances which in its opinion exist and which in its opinion suggest an intent to defraud or a fraudulent or unlawful purpose. It is equally unreasonable to think that the Legislature could have abandoned even the small safeguard of requiring the opinion to be founded on existent circumstances which suggest the things for which an investigation can be ordered and left the opinion and even the existence of circumstances from which it is to be formed to a subjective process…

If it is shown that the circumstances do not exist or that they are such that it is impossible for any one to form an opinion therefrom suggestive of the aforesaid things, the opinion is challengeable on the ground of non-application of mind or perversity or on the ground that it was formed on collateral grounds and was beyond the scope of the statute’.

Hidayathullah, J. in his concurring opinion stated (page 661) :

‘No doubt, the formation of opinion is subjective but the existence of circumstances relevant to the inference as the sine qua non for action must be demonstrable. If the action is question on the ground that no circumstances leading to an inference of the kind contemplated by the section exists, the action might be exposed to interference unless the existence of the circumstances is made out. . . .’" (p. 124)

The principle equally applies to the formation of reason to believe that income has escaped the assessment. The requirement of recording of reason before issuance of notice is to provide safeguard against the arbitrary action that may be taken by reopening the completed assessment time and again on irrelevant consideration. Recording of reasons unfolds the process by which the Assessing Officer was led to formation of his belief about escapement of income. If the action of the Assessing Officer is founded on some material or ground that has no nexus to the formation of reason to believe or is not founded on any existing material, the same is liable to be interfered with. Recording of reasons opens window to the process by which the Assessing Officer reaches his belief, in case the action is challenged, to enable the Court to find out whether he has formed his belief on the relevant material or grounds which have some nexus to the tentative opinion which he has formed. The correctness of his tentative opinion is not be tested on the anvil of final decision which may be reached after considering the rival contentions and weighing them through the process of reasoning. But at the same time, if it appears from the reasoning which has been adopted by the Assessing Officer that no inference of escapement of income from assessment can at all be drawn therefrom, it must be held that the action is ultra vires the statute and does not confer jurisdiction on the Assessing Officer to act on that basis.”

2.2. What is the significance of omission of the phrase “reason to believe.” Parliament, while exercising legislative function, when omits a particular phrase, it does so consciously and presumably, intentionally and hence some meaning has to be assigned to such omission. The logical corollary is that instead of belief of the AO which could be tentative or prima facie, now escapement has to be established before issuance of notice of reopening. Belief is subjective however, based on some objective criterial. It is to a great extent a matter of perception. As against the same, escapement is a matter of fact and needs solid evidences to establish. So apparently now the burden is more on the revenue before issuance of notice u/s 148 of the Act. The distinction is aptly explained by Hon’ble Supreme Court in the case of ACIT vs Rajesh Jhaveri Stock Brokers (P.) Ltd. [2007] 291 ITR 500 (SC) wherein it was held thus:

“16. Section 147 authorises and permits the Assessing Officer to assess or reassess income chargeable to tax if he has reason to believe that income for any assessment year has escaped assessment. The word "reason" in the phrase "reason to believe" would mean cause or justification. If the Assessing Officer has cause or justification to know or suppose that income had escaped assessment, it can be said to have reason to believe that an income had escaped assessment. The expression cannot be read to mean that the Assessing Officer should have finally ascertained the fact by legal evidence or conclusion. The function of the Assessing Officer is to administer the statute with solicitude for the public exchequer with an inbuilt idea of fairness to taxpayers. As observed by the Supreme Court in Central Provinces Manganese Ore Co. Ltd. v. ITO [1991] 191 ITR 662, for initiation of action under section 147(a) (as the provision stood at the relevant time) fulfilment of the two requisite conditions in that regard is essential. At that stage, the final outcome of the proceeding is not relevant. In other words, at the initiation stage, what is required is "reason to believe", but not the established fact of escapement of income. At the stage of issue of notice, the only question is whether there was relevant material on which a reasonable person could have formed a requisite belief. Whether the materials would conclusively prove the escapement is not the concern at that stage. This is so because the formation of belief by the Assessing Officer is within the realm of subjective satisfaction ITO v. Selected Dalurband Coal Co. (P.) Ltd. [1996] 217 ITR 597 (SC); Raymond Woollen Mills Ltd. v. ITO [1999] 236 ITR 34 (SC).”

Validity of other items of addition in a reassessment without adding the very item which was the ground for reopening.

2.3. Explanation to S. 147 gives power to AO to assess the income in respect of any issue other than what is stated in the reasons. In other words, once an assessment is validly reopened, the same would be at large before the AO and items other than subject matter of reasons can also be covered in such reassessment proceedings. An interesting issue, however, may arise with respect to fate of other additions when the very item which was the ground for reopening is not added in the final reassessment order. Under the old regime this issue is well settled [CIT vs Jet Airways (I) Ltd 331 ITR 236 (Bom)]. In order to answer this issue under the new regime, one will have to compare the provisions of S. 147 under the old and new regime:

Old Act: S.147. If the Assessing Officer has reason to believe that any income chargeable to tax has escaped assessment for any assessment year, he may, subject to the provisions of sections 148 to 153, assess or reassess such income and also any other income chargeable to tax which has escaped assessment and which comes to his notice subsequently in the course of the proceedings under this section, or re-compute the loss or the depreciation allowance or any other allowance, as the case may be, for the assessment year concerned (hereafter in this section and in sections 148 to 153 referred to as the relevant assessment year) :

Existing Act: S.147. If any income chargeable to tax, in the case of an assessee, has escaped assessment for any assessment year, the Assessing Officer may, subject to the provisions of sections 148 to 153, assess or reassess such income or recompute the loss or the depreciation allowance or any other allowance or deduction for such assessment year (hereafter in this section and in sections 148 to 153 referred to as the relevant assessment year).

2.4. On first blush it seems that there is no compulsion on AO to add the item that is the subject matter of grounds for reopening and only then add other items. However, upon close scrutiny, it would be clear that if such an item is not added, there cannot be an escapement of income chargeable to tax at all and therefore, such an order must fail. As regards the absence of the phrase “such income and also any other income” under the new regime, the rationale is in the difference in both the schemes. As discussed hereinabove, earlier reopening power could be exercised when the AO had ‘reason to believe’ that income has escaped assessment. Such belief of the AO is tentative or prima facie, and therefore may not culminate into an actual addition when reassessment order is framed. Hence legislature put an additional check by inserting this conditional phrase that other additions could be made only if the item that is the subject matter of grounds for reopening is added. However, under the new regime, the factum of income having escaped assessment has to be established before issuance of notice of reopening and therefore an eventuality of that very item being not added in the final reassessment order is not contemplated by the legislature. However, if such an order is passed, the same would be treated as bad in law as there is no escapement at all.

Principles of Merger after deletion of 3rd proviso to old S.147.

2.5. 3rd Proviso to old S. 147 of the Act that provided for exclusion of matters which are subject matters of any appeal, reference or revision from the purview of reassessment, not stands deleted. There is no provision analogous to this proviso in the new scheme. However, principles of merger can be pressed into service when an issue that was the subject matter of appeal, having been decided and the same is now sought to be reopened. When an order is challenged in appeal or by way of revision, the original order merges into the order of the appellate or revisionary authority upon passing of the order by respective authority and hence beyond the scope of reopening by AO. However, mere pendency of appeal cannot be saved by principle of merger.

Effect of deletion of Explanation 2 – Deemed Escapement

2.6. Under the new scheme, there is no concept of deemed escapement as existed under Explanation 2 to S. 147 of the Act under the old scheme. This exclusion is going to create certain interesting issues. Explanation 2 defines deemed escapement of income or presumption as regards escapement where apparently there is none. Concept of escapement is sine qua non for reopening, both under the old as well as new schemes. The fact that the situations prescribed under Explanation 2 do not involve escapement is evident from the very existence of the said provision under the old Act. If those situations involved escapement, there was no need for a deeming fiction under the old Act also. Therefore, in absence of the said Explanation 2 under the new scheme, it would always remain open to the assessee to plead that there is no presumption as regards escapement under the situations prescribed therein and hence reopening is not permissible for want of escapement.

3. Section 148: Issue of notice where income has escaped assessment.

Before making the assessment, reassessment or recomputation under section 147, and subject to the provisions of section 148A, the Assessing Officer shall serve on the assessee a notice, along with a copy of the order passed, if required, under clause (d) of section 148A, requiring him to furnish within such period, as may be specified in such notice, a return of his income or the income of any other person in respect of which he is assessable under this Act during the previous year corresponding to the relevant assessment year, in the prescribed form and verified in the prescribed manner and setting forth such other particulars as may be prescribed; and the provisions of this Act shall, so far as may be, apply accordingly as if such return were a return required to be furnished under section 139:

Provided that no notice under this section shall be issued unless there is information with the Assessing Officer which suggests that the income chargeable to tax has escaped assessment in the case of the assessee for the relevant assessment year and the Assessing Officer has obtained prior approval of the specified authority to issue such notice.

Provided further that no such approval shall be required where the Assessing Officer, with the prior approval of the specified authority, has passed an order under clause (d) of section 148A to the effect that it is a fit case to issue a notice under this section.

Explanation 1.—For the purposes of this section and section 148A, the information with the Assessing Officer which suggests that the income chargeable to tax has escaped assessment means,—

|

(i) |

|

any information in the case of the assessee for the relevant assessment year in accordance with the risk management strategy formulated by the Board from time to time; |

|

(ii) |

|

any audit objection to the effect that the assessment in the case of the assessee for the relevant assessment year has not been made in accordance with the provisions of this Act; or |

|

(iii) |

any information received under an agreement referred to in section 90 or section 90A of the Act; or |

|

|

(iv) |

any information made available to the Assessing Officer under the scheme notified under section 135A; or |

|

|

(v) |

any information which requires action in consequence of the order of a Tribunal or a Court. |

Explanation 2.—For the purposes of this section, where,—

|

(i) |

|

a search is initiated under section 132 or books of account, other documents or any assets are requisitioned under section 132A, on or after the 1st day of April, 2021, in the case of the assessee; or |

|

(ii) |

|

a survey is conducted under section 133A, other than under sub-section (2A) of that section, on or after the 1st day of April, 2021, in the case of the assessee; or |

|

(iii) |

|

the Assessing Officer is satisfied, with the prior approval of the Principal Commissioner or Commissioner, that any money, bullion, jewellery or other valuable article or thing, seized or requisitioned under section 132 or section 132A in case of any other person on or after the 1st day of April, 2021, belongs to the assessee; or |

|

(iv) |

|

the Assessing Officer is satisfied, with the prior approval of Principal Commissioner or Commissioner, that any books of account or documents, seized or requisitioned under section 132 or section 132A in case of any other person on or after the 1st day of April, 2021, pertains or pertain to, or any information contained therein, relate to, the assessee, |

the Assessing Officer shall be deemed to have information which suggests that the income chargeable to tax has escaped assessment in the case of the assessee where the search is initiated or books of account, other documents or any assets are requisitioned or survey is conducted in the case of the assessee or money, bullion, jewellery or other valuable article or thing or books of account or documents are seized or requisitioned in case of any other person.

Explanation 3.—For the purposes of this section, specified authority means the specified authority referred to in section 151.

3.1. S. 148(2) prior to its deletion wef 01/04/2021 reads thus “The Assessing Officer shall, before issuing any notice under this section, record his reasons for doing so”. Now the prior requirement of recoding the reasons before issuance of notice u/s 148 of the Act is done away with. Order u/s 148A(d) of the Act itself will be treated as reasons. Other important features of the new section are as under:

· Notice u/s 148 of the Act should be served along with a copy of the order passed u/s 148A(d) if required.

· Unless there is information which suggests escapement of income chargeable to tax with the AO, he cannot issue notice u/s 148 of the Act.

· Action should be taken with prior approval of the specified authority as prescribed u/s 151 of the Act.

Meaning of ‘Information’ which ‘suggests’ escapement of income chargeable to tax.

3.2. In absence of definition of the word ‘information’ under the old law governing reopening, the word ‘information’ came up for consideration before Hon’ble Supreme Court in numerous judgments. In the case of CIT vs. A. Raman & Co. [1968] 67 ITR 11 (SC), Hon’ble Supreme Court held that:

“The expression “information” in the context in which it occurs must, in our judgment, mean instruction or knowledge derived from an external source concerning facts or particulars, or as to law relating to a matter bearing on the assessment.”

“Information in his possession that income chargeable to tax has escaped assessment furnishes a starting point, for assessing or reassessing income.”

3.3. In the case of Maharaj Kumar Kamal Singh vs. CIT [1959] 35 ITR 1 (SC), notice u/s.34 of the 1922 Act was issued subsequent to overturning of Patna High Court decision that the assessee had relied upon in the assessment and appeal proceedings. Assessee argued that information can only constitute factual information. It was held that:

“If the word "information" in its plain grammatical meaning includes information as to facts as well as information as to the state of the law, it would be unreasonable to limit it to information as to the facts on the extraneous consideration that some cases of assessment which need to be revised or rectified on the ground of mistake of law may conceivably be covered by sections 33B and 35.”

“…the belief of the Income-tax Officer that any given income has been assessed at too low a rate may in many cases be due to information about the true legal position in the matter of the relevant rates. If the word "information" in reference to this class of cases must necessarily include information as to law, it is impossible to accept the argument that, in regard to the other cases falling under the same provision, the same word should have a narrower and a more limited meaning. We would accordingly hold that the word "information" in section 34(1)(b) includes information as to the true and correct state of the law and so would cover information as to relevant judicial decisions.”

3.4. The phrase “information with the Assessing Officer which suggests that the income chargeable to tax has escaped assessment” used in the first proviso to S. 148 has to be interpreted keeping in mind the implications of the word “suggests”. The word ‘suggest’ is not defined under the Act. Therefore one has to fallback upon the general dictionary meaning of the same:

“to call to mind by thought or association” Merriam-Webster

“If one thing suggests another, it implies it or makes you think that it might be the case.” Collins Dictionary

So ‘suggest’ seems to be suggesting that there should be a live and direct nexus between the information and the income chargeable to tax escaping assessment.

3.5. Explanation 1 defines ‘information with the Assessing Officer which suggests that the income chargeable to tax has escaped assessment’. Originally, there were only two clauses. However, wef 01/04/2022, parliament introduced 3 more clauses so now there are 5 clauses clarifying what is information.

3.6. It may be noted that explanation one does not defined only ‘information’, it defines suggestive information as regards income chargeable to tax escaping assessment. In other words ‘information’ comes with built suggestions of escapement of income.

3.7. Clause (i) talks about information emanating from the risk management strategy formulated by the Central Board of Direct Taxes (“CBDT” for short) from time to time. Wef 01/04/2022 the word ‘flagged’ has been omitted. Flagged information means only filtered information and not all information. However, omission of the term ‘flagged’ means every information collected as per the risk management strategy could be used to initiate reassessment. This to a great extent reduces the objectivity in the procedure. Based on the obligation cast upon various persons u/s.285BA of the Act and such other provisions whereby information is collected and processed for formulating dynamic risk management strategy, CBDT came out with Instruction dated December 10, 2021 bearing no F.N0. 225/135/2021/ITA-II which is reproduced for ready reference:

“SECTION 119 OF THE INCOME-TAX ACT, 1961 – CENTRAL BOARD OF DIRECT TAXES – INSTRUCTION TO SUBORDINATE AUTHORITIES – INSTRUCTION REGARDING UPLOADING OF INFORMATION ON VRU FUNCTIONALITY ON INSIGHT PORTAL FOR IMPLEMENTATION OF RISK MANAGEMENT STRATEGY FOR ISSUE OF NOTICE UNDER SECTION 148

INSTRUCTION F. NO. 225/135/2021/ITA-II, DATED 10-12-2021

Kindly refer to the above.

2. As per the amended provisions of the section 148 of the Income-tax Act,1961('the Act'), the information which has escaped assessment has been defined to include the two categories of information, i.e., (i) the information which is flagged in accordance with the risk management strategy formulated by the Board; and (ii) final audit objection raised by the C&AG.

3. For effective implementation of risk management strategy, the Central Board of Direct Taxes (Board), in exercise of its powers under section 119 of the Act, directs that the Assessing Officers shall identify the following categories of information pertaining to Assessment Year 2015-16 and Assessment Year 2018-19, which may require action under section 148 of the Act, for uploading on the Verification Report Upload (VRU) functionality on Insight portal:

|

(i) |

|

Information from any other Government Agency/Law Enforcement Agency |

|

(ii) |

|

Information arising out of Internal Audit objection, which requires action u/s 148 of the Act |

|

(iii) |

|

Information received from any Income-tax Authority including the assessing officer himself or herself |

|

(iv) |

|

Information arising out of search or survey action |

|

(v) |

|

Information arising out of FT&TR references |

|

(vi) |

|

Information arising out of any order of court, appellate order, order of NCLT and/or order u/s 263/264 of the Act, having impact on income in the assessee's case or in the case of any other assessee |

|

(vii) |

|

Cases involving addition in any assessment year on a recurring issue of law or fact: |

|

a. |

|

exceeding Rs. 25 lakhs in eight metro charges at Ahmedabad, Bengaluru, Chennai, Delhi, Hyderabad, Kolkata, Mumbai and Pune while at other charges, quantum of addition should exceed Rs. 10 lakhs; |

|

b. |

|

exceeding Rs. 10 crore in transfer pricing cases. |

and where such an addition:

|

1. |

|

has become final as no further appeal has been filed against the assessment order; or |

|

2. |

|

has been confirmed at any stage of appellate process in favor of revenue and assessee has not filed further appeal; or |

|

3. |

|

has been confirmed at the 1st stage of appeal in favor of revenue or subsequently; even if further appeal of assessee is pending, against such order. |

5. As per the provisions of section 149(1)(b) of the Act, in specific cases where the Assessing Officer has in his possession evidence which reveal that the income escaping assessment, represented in the form of asset, amounts to or is likely to amount to fifty lakh rupees or more, notice can be issued beyond the period of three years but not beyond the period of ten years from the end of the relevant assessment year. Further, the notice under section 148 of the Act cannot be issued at any time in a case for the relevant assessment year beginning on or before 1st day of April, 2021, if such notice could not have been issued at that time on account of being beyond the time limit prescribed under the provisions of clause (b), as they stood immediately before the proposed amendment. As per explanation provided to section 149 of the Act, the term "asset" shall include immovable property, being land or building or both, shares and securities, loans and advances, deposits in bank account.

5.1 In view of the above, it is directed that the information pertaining to Assessment Year 2015-16, which requires action u/s 148 of the Act shall be identified and uploaded on the VRU functionality on insight portal only as per the provisions of section 149(1)(b) of the Act.

6. The above exercise of identifying and uploading the information along with the underlying documents in the above categories of cases must be completed by 20-12-2021.

7. These Instructions shall be applicable to the Jurisdictional Assessing Officers and Assessing Officers of Central Charges and International Taxation.

8. The above Instructions may be brought to the notice of the officers concerned under your region.

9. This issues with the approval of Chairman, CBDT.

(Ravieder Maini)

Director (ITA-II), CBDT

■■”

The above instruction is indicative of the way in which ‘information’ is going to be collected, processed and most importantly given a very wide meaning. In times to come, based on the feedback from the field officers and analysis of the data mined with the help of artificial intelligence algorithms, CBDT will notify diverse criteria as ‘information’ for various years.

In view of Hon’ble Supreme Court’s judgment in the case of Union of India & Ors. Vs Ashish Agarwal (Civil Appeal No.3005/2022 dated 04/05/2022, copy annexed with this paper), notice issues between 01/04/2021 to 30/06/2021 would be treated as deemed notices u/s 148A(b) of the Act. Most of these notices were issued based on information from 4 sources, viz.: (i) from other AOs, (ii) from other agencies, (iii) from investigation wing and (iv) insight portal. Other than the information received from the Insight Portal no other source qualifies for the criterion of flagged in accordance with the risk management strategy. Would the AO be allowed to proceed in these cases where information is not flagged in accordance with the risk management strategy as the same would not be treated as ‘information’ at all?

3.8. Clause (ii) states that any audit objection (as against final audit objection and that too only by the C&AG of India from 01/04/2021 to 31/03/2022) to the effect that assessment has not been made in accordance with the provisions of the Act. Reopening pursuance to audit objection has always been a bone of contention between the department and assessee. However, for the first time, audit objection is part of the statutory provision to enable AO to initiate reopening based on audit objection. In the case of Indian & Eastern Newspaper Society vs. CIT [1979] 119 ITR 996 (SC) internal audit party of the IT Department expressed the view that income of the assessee newspaper association on account of occupation of conference halls should not have been assessed as income from business but ought to have been assessed as income from house property. ITO treated this as “information” and reassessed income. Hon’ble Supreme Court held thus:

“…when section 147(b) of the Income-tax Act is read as referring to "information" as to law, what is contemplated is information as to the law created by a formal source.”

“the ITO had, when he made the original assessment, considered the provisions of sections 9 and 10. Any different view taken by him afterwards on the application of those provisions would amount to a change of opinion on material already considered by him.”

“Plainly, the statutory provision envisages that the ITO must first have information in his possession, and then in consequence of such information he must have reason to believe that income has escaped assessment. The realisation that income has escaped assessment is covered by the words "reason to believe", and it follows from the "information" received by the ITO. The information is not the realisation, the information gives birth to the realisation.”

“…the opinion of an internal audit party of the Income-tax Department on a point of law cannot be regarded as "information" within the meaning of section 147(b) of the Income-tax Act, 1961.”

3.9. Gujarat High Court in the case of Adani Infrastructure & Developers (P.) Ltd. v. ACIT [2019] 101 taxmann.com 256 (Guj) had an occasion to deal with one such issue. In the facts of that case assessment was sought to be reopened based on audit party objection w.r.t. s.14A disallowance. Audit file revealed that AO had not accepted the objections raised by the audit party and had stated that after considering the applicability of section 14A of the Act, he was satisfied with the disallowance. Hon’ble Court held that:

“Evidently therefore, the Assessing Officer has not formed any independent belief that the income chargeable to tax has escaped assessment and on the contrary has stated that he had considered the applicability of provisions of section 14A of the Act and was satisfied in adopting 0.5% of average value of investment for disallowance under section 14A of the Act.”

“It is by now well settled that the assessment cannot be reopened merely on the basis of an audit report without the Assessing Officer independently forming the belief, may be on the basis of such report, that income chargeable to tax has escaped assessment. The above referred decision would, therefore, be squarely applicable to the facts of the present case. The impugned notice issued by the respondent under section 148 of the Act being based merely upon the audit objection and not because the Assessing Officer had reason to believe that any income chargeable to tax has escaped assessment, cannot be sustained.”

3.10. Before Hon’ble Madras High Court in the case of CIT vs. Lucas T.V.S. Ltd. [1998] 234 ITR 296 (Madras) controversy arose in light of the fact that in the original assessment, the assessee claimed the entire expenditure for construction of a building as capital expenditure for scientific research u/s.35(2) of the Act in the year of completion. The assessment was reopened on the basis of an audit objection that only the expenditure incurred in the relevant previous year would be allowable. Hon’ble Court held that:

“As per the decision of the Supreme Court in Indian and Eastern Newspaper Society v. CIT [1979] 119 ITR 996, an audit opinion in regard to the application or interpretation of law cannot be treated by the Income-tax Officer as information for reopening the assessment under section 147(b) of the Act.”

“Apart from the information furnished by the audit party, the Income-tax Officer has no other information for reopening the assessment as can be seen from the reasons recorded by him for reopening the assessment under section 147(b) of the Act. The opinion expressed by the audit party would go to show that they have pointed out to the Income-tax Officer that he failed to apply the provisions contained in section 35 of the Act to the facts arising in this case. This would amount to pointing out the law and the interpretation of the provisions contained in section 35, which is clearly barred by the decision of the Supreme Court in Indian and Eastern Newspaper Society v. CIT [1979] 119 ITR 996, for reopening the assessment under section 147(b) of the Act.”

This decision was confirmed by the Hon’ble SC in [2001] 249 ITR 306 (SC).

3.11. Now, audit objection itself is considered as ‘information’ based on which reopening proceedings can be initiated. However, issues with respect to live nexus between the audit objections and escapement of income, the exclusive jurisdiction of AO to reopen and legal and/or factual issues having already been examined at the original stage by the AO could still be raised as valid defenses in a challenge to reopening.

3.12. Clauses (iii), (iv) and (v) are all based on internal or external source based information which could give a fresh cause of action to reopen indiscriminately and without exception. Insertion of these additional clauses makes it obligatory on the part of the AO to reopen the cases of assessee whose reported transactions are at variance with the information available with the Department or based on any conflicting decision of the Tribunal or Court even in cases of other assessees.

When AO shall be ‘Deemed’ to have Information which suggests escapement of income chargeable to tax.

3.13. Explanation 2 defines what is deemed information. All the cases of search u/s 132, requisition u/s 132A, survey u/s 133A (other than TDS survey u/s 133(2A) and third party search and requisition (falling under earlier provisions of S.153C of the Act) taking place after 01/04/2021 would be covered under this deeming provision enabling the AO to issue notices u/s 148 without having to bring on record any information. Here search and survey itself would be construed as information suggestive of escapement of income. The deeming fiction creates a presumption as regards existence of information suggesting escapement of income even when specific information vis-à-vis a particular Assessee or a particular Assessment year may not be available. This explanation enables the revenue to presume that there is an actionable information suggestive of escapement of income available for initiating actions under section 148 even when no such information exists.

Period of reopening – in the cases of Search & Survey

3.14. Between 01/04/2021 to 31/03/2022, such deemed information under Explanation 2 was available only for a period of 3 years immediately preceding the assessment year relevant to the previous year in which search is initiated. However, after 01/04/2022, the presumption as regards deemed information is not restricted to 3 years. It could be for as long as 10 years. What is worse is the fact that search cases are excluded from the purview of S.148A of the Act and therefore even for the years covered u/s 149(1)(b) (i.e. 4th to 10th year), where reopening is subject to fulfilment of certain conditions, there would be automatic reopening without any order u/s 148A(d). So the assessee would not even know the reason for reopening for these years!

Inter-play between S. 147 and S. 148

3.15. S. 147 of the Act is the jurisdictional section. Fulfilment of the conditions prescribed under this section empowers the AO to assume jurisdiction to reopen. S. 148 on the other hand, is the procedural section which prescribes modalities for issuance of notice if the test of jurisdiction u/s 147 is passed. For S. 147, it is only escapement of income which is a sine qua non. However, suggestive information is not at all required for assuming jurisdiction u/s 147 of the Act. Therefore, availability of information with the AO which suggests that the income chargeable to tax has escaped assessment for the relevant assessment year is an additional condition for issuance of notice u/s 148 of the Act. The argument that “reasons to believe” has given the way to “information with the assessing officer which suggests that the income chargeable to tax has escaped assessment” under the new regime is fallacious. For assuming jurisdiction u/s 147 of the Act under the new regime there must be an escapement of income, not just a belief of the AO that income has escaped assessment. Escapement is further qualified u/s 148 to the effect that such escapement must emanate from information as prescribed u/s 148 of the Act. Here the derivation of escapement based on the information could be suggestive, which can be subjective. However, ‘reason to believe’ is not at all replaced with ‘information that suggests escapement’.

Deemed Escapement vs Information which suggests that the income chargeable to tax has escaped assessment”

3.16. ‘Deemed Escapement’ as defined in Explanation 2 to old S.147 of the Act has the effect of presumption of escapement and since it was part of the old jurisdictional section, such presumption would confer jurisdiction on the AO. As against the same, Explanation 1 to S. 148 deals with specific information which suggests that a transaction for a relevant year vis-à-vis an assessee has escaped assessment so reopening can be initiated if suggestive information can result into escapement of income as required u/s 147 of the Act. Explanation 2 to S. 148 goes one step further and creates a deeming fiction in as much as whenever there is search/survey action, the existence of information suggestive of escapement of income would be presumed for all the years falling within the period of limitation. However, the same is not equal to deemed escapement. What is presumed by deeming fiction is availability of information suggestive of escapement of income for the entire period. But the same is not deemed escapement as existed under the old Act.

4. Section 148A: Conducting inquiry, providing opportunity before issue of notice under section 148.

The Assessing Officer shall, before issuing any notice under section 148,—

|

(a) |

|

|

conduct any enquiry, if required, with the prior approval of specified authority, with respect to the information which suggests that the income chargeable to tax has escaped assessment; |

|

(b) |

|

|

provide an opportunity of being heard to the assessee, by serving upon him a notice to show cause within such time, as may be specified in the notice, being not less than seven days and but not exceeding thirty days from the date on which such notice is issued, or such time, as may be extended by him on the basis of an application in this behalf, as to why a notice under section 148 should not be issued on the basis of information which suggests that income chargeable to tax has escaped assessment in his case for the relevant assessment year and results of enquiry conducted, if any, as per clause (a); |

|

(c) |

|

|

consider the reply of assessee furnished, if any, in response to the show-cause notice referred to in clause (b); |

|

(d) |

|

|

decide, on the basis of material available on record including reply of the assessee, whether or not it is a fit case to issue a notice under section 148, by passing an order, with the prior approval of specified authority, within one month from the end of the month in which the reply referred to in clause (c) is received by him, or where no such reply is furnished, within one month from the end of the month in which time or extended time allowed to furnish a reply as per clause (b) expires: |

Provided that the provisions of this section shall not apply in a case where,—

|

(a) |

|

a search is initiated under section 132 or books of account, other documents or any assets are requisitioned under section 132A in the case of the assessee on or after the 1st day of April, 2021; or |

|

(b) |

|

the Assessing Officer is satisfied, with the prior approval of the Principal Commissioner or Commissioner that any money, bullion, jewellery or other valuable article or thing, seized in a search under section 132 or requisitioned under section 132A, in the case of any other person on or after the 1st day of April, 2021, belongs to the assessee; or |

|

(c) |

|

the Assessing Officer is satisfied, with the prior approval of the Principal Commissioner or Commissioner that any books of account or documents, seized in a search under section 132 or requisitioned under section 132A, in case of any other person on or after the 1st day of April, 2021, pertains or pertain to, or any information contained therein, relate to, the assessee; or |

|

(d) |

|

the Assessing Officer has received any information under the scheme notified under section 135A pertaining to income chargeable to tax escaping assessment for any assessment year in the case of the assessee. |

Explanation.—For the purposes of this section, specified authority means the specified authority referred to in section 151.

4.1. With the introduction of S. 148A of the Act, the law laid down by the decision of GKN Drive Shaft is now legislated. Hon’ble Supreme Court in the case of GKN Driveshafts (India) Ltd. v. ITO 259 ITR 19 (SC) has held that:

“However, we clarify that when a notice under section 148 of the Income Tax Act is issued, the proper course of action for the noticee is to file return and if he so desires, to seek reasons for issuing notices. The Assessing Officer is bound to furnish reasons within a reasonable time. On receipt of reasons, the noticee is entitled to file objections to issuance of notice and the Assessing Officer is bound to dispose of the same by passing a speaking order.”

This judgement was further refined and a timeline for the above stated process was laid down in Sahkari Khand Udyog Mandal Ltd. vs. ACIT [2015] 370 ITR 107 (Guj). Now this whole process has been made a part of S.148A of the Act.

Procedure under clauses (a) to (d) of section 148A of the Act

4.2. Clause (a) to S.148A contemplates pre-notice inquiry if required, with respect to the information which suggests that the income chargeable to tax has escaped assessment with the prior approval of specified authority specified.

4.3. As per clause (b) to S.148A, assessee concerned must be given an opportunity of hearing. A show cause notice is required to be served upon the assessee giving him at least 7 days to respond to the proposed action of reopening.

Notice under clause (b) needs to be served properly

“Show cause notice” under “clause (b)” of “section 148A” of the Act is required to be “served” upon the assessee in accordance with the scheme of the Act. Mere “issuance” of such show cause notice is not sufficient since Legislature has consciously provided for “service” of show cause notice as against mere “issuance” of notice. Further, service of any notice, including notice under clause (b) of section 148A of the Act, must be effected in accordance with the provisions of section 282 of the Act read with Rule 127 of The Income Tax Rules, 1962. Since faceless reassessment Scheme as notified on 29/03/2022 states that provisions of S.144B of the Act to the extent provided for are also applicable, it is necessary to examine the provisions of service under the said Scheme. Section 144B (viz. Faceless Assessment) provides that “every notice or order or any other electronic communication” shall be delivered to the assessee concerned in the manner prescribed therein and followed by a real time alert.

The term “real time alert” means any communication sent to the assessee, by way of –

Ø short messaging service on his registered mobile number; or

Ø update on his mobile app; or

Ø an email at his registered email address;

so as to alert him regarding delivery of an electronic communication.

4.4. A conjoint reading of the above discussed provisions would indicate that notice under clause (b) of section 148A of the Act has to be served upon the assessee concerned in the manner prescribed in the scheme of the Act. If such notice is not served in the said manner, then such notice is not tenable in the eye of law. Accordingly, all the consequential proceedings would also not be tenable in the eye of law.

4.5. Another facet of principles of natural justice is also worth discussing here. Reasonable time has to be granted to the assessee to furnish reply in response to the show cause notice under clause (b) of section 148A of the Act. Legislature has prescribed “minimum period of 7 days” and “maximum period of 30 days” for furnishing reply to the show cause notice issued under clause (b) of section 148A of the Act to begin with. Maximum time of 30 days can be extended in an appropriate case by the AO is application to that effect is filed by the Assessee.

4.6. After considering material available on record including reply of the assessee, the AO may pass an order under clause (d) of S.148A of the Act by passing a speaking order within a period of one month from the end of the month in which reply of the assessee is received by him determining whether or not it is a fit case to issue a notice for assessment / re-assessment / re-computation. When no reply is furnished, AO should pass an order under cluse (d) with a period of one month from the end of the month in which time to furnish reply as per clause (b) expires. These time limits are mandatory and any deviation from the same would vitiate the proceedings.

4.7. This process of enquiry and adjudication u/s 148A shall not apply to any issue which comes to the notice of the AO subsequently in the course of reassessment proceedings u/s 147 of the Act.

Exception to procedure prescribed u/s 148A

4.8. Proviso to S. 148A carves out exceptions to applicability of S. 148A procedure. As per the proviso all the cases of search u/s 132, requisition u/s 132A, third party search and requisition (falling under earlier provisions of S.153C of the Act) taking place after 01/04/2021 and cases of AO receiving information pursuant to scheme notified u/s 135A would be covered under this exception and the procedure of S. 148A of the Act is not required to be fulfilled for those cases. S. 135A provides for faceless collection of information under specified sections within the department. No scheme has been notified so far and it is unclear as to what incremental information the department would have u/s 135A when the same is available in Insight portal. What is more disturbing however, is the fact that initiation of reassessment on the basis of information available u/s 135A of the Act is not subject to the provisions of S. 148A which provides an opportunity to the assessee to defend the initiation of proceedings at the outset by making necessary submissions. Even the order u/s 148A(d) of the Act would not be passed in such cases resulting into depriving the assessee of the reasons for reopening.

It may be noted that this proviso does not cover survey cases and therefore 148A procedure needs to be followed in case of reopening as a result of survey.

Challenge to order u/s 148A(d) read with notice u/s 148 of the Act.

4.9. Since order u/s 148A(d) is not an appealable order, only writ can be filed against such order if assessee is aggrieved by such order and consequential notice u/s 148 of the Act. Delhi High Court in the case of Gulmuhar Silk Pvt. Ltd. ( W.P.(C) 5787/2022) dismissed the writ petition filed by the assessee challenging reopening under the new regime on the ground of availability of alternate remedy. However, when an order is passed in gross violation of principles of natural justice or not in accordance with law or the same is patently bad, illegal and without jurisdiction, Hon’ble High Court under Article 226, can certainly entertain writ petition even if alternate remedy of appeal is available. An assessee cannot be made to go through the entire gamut of appellate proceedings when a jurisdictional notice is inherently illegal and without jurisdiction. Under such circumstances, the alternate remedy though available, is not an efficacious remedy. (Reference: Calcutta Discount Co. vs ITO [41 ITR 191 (SC) @ 207-208, para 26-27-28] & Whirlpool Corporation vs Registrar of Trade Marks [(1998) 8 SCC 1, para 14 & 15].

5. Section 148B: Prior approval for assessment, reassessment or recomputation in certain cases.

No order of assessment or reassessment or recomputation under this Act shall be passed by an Assessing Officer below the rank of Joint Commissioner, in respect of an assessment year to which clause (i) or clause (ii) or clause (iii) or clause (iv) of Explanation 2 to section 148 apply except with the prior approval of the Additional Commissioner or Additional Director or Joint Commissioner or Joint Director.”.

5.1. In the cases related to Search and Survey as mentioned in Explanation 2 to S.148 of the Act, assessment order should be passed by an officer in or above the rank of Jt. Commissioner that too with the prior approval of Additional Commissioner or Additional Director or Joint Commissioner or Joint Director. It goes without saying that if the order in question itself is passed by the sanctioning authority mentioned hereinabove or any higher authority, no approval as contemplated u/s 148B would be required.

6. Section 149: Time limit for notice.

(1) No notice under section 148 shall be issued for the relevant assessment year,—

|

(a) |

|

if three years have elapsed from the end of the relevant assessment year, unless the case falls under clause (b); |

|

(b) |

|

if three years, but not more than ten years, have elapsed from the end of the relevant assessment year unless the Assessing Officer has in his possession books of account or other documents or evidence which reveal that the income chargeable to tax, represented in the form of–– (i) an asset; (ii) expenditure in respect of a transaction or in relation to an event or occasion; or (iii) an entry or entries in the books of account,

|

Provided that no notice under section 148 shall be issued at any time in a case for the relevant assessment year beginning on or before 1st day of April, 2021, if a notice under section 148 or section 153A or section 153C could not have been issued at that time on account of being beyond the time limit specified under the provisions of clause (b) of sub-section (1) of this section or section 153A or section 153C, as the case may be, as they stood immediately before the commencement of the Finance Act, 2021:

Provided further that the provisions of this sub-section shall not apply in a case, where a notice under section 153A, or section 153C read with section 153A, is required to be issued in relation to a search initiated under section 132 or books of account, other documents or any assets requisitioned under section 132A, on or before the 31st day of March, 2021:

Provided also that for the purposes of computing the period of limitation as per this section, the time or extended time allowed to the assessee, as per show-cause notice issued under clause (b) of section 148A or the period during which the proceeding under section 148A is stayed by an order or injunction of any court, shall be excluded:

Provided also that where immediately after the exclusion of the period referred to in the immediately preceding proviso, the period of limitation available to the Assessing Officer for passing an order under clause (d) of section 148A is less than seven days, such remaining period shall be extended to seven days and the period of limitation under this sub-section shall be deemed to be extended accordingly.

Explanation.—For the purposes of clause (b) of this subsection, "asset" shall include immovable property, being land or building or both, shares and securities, loans and advances, deposits in bank account.

(1A) Notwithstanding anything contained in sub- section (1), where the income chargeable to tax represented in the form of an asset or expenditure in relation to an event or occasion of the value referred to in clause (b) of sub-section (1), has escaped the assessment and the investment in such asset or expenditure in relation to such event or occasion has been made or incurred, in more than one previous years relevant to the assessment years within the period referred to in clause (b) of sub-section (1), a notice under section 148 shall be issued for every such assessment year for assessment, reassessment or recomputation, as the case may be.

(2) The provisions of sub-section (1) as to the issue of notice shall be subject to the provisions of section 151.

6.1. S. 149 of the Act prescribes time limits for issuance of notice u/s 148 of the Act. Here the legislature uses the word ‘issued’ and not served. In interpreting the word “issued’ courts have held that notice can be said has been issued when the same is given to independent agent for service. Section prescribes that notice must be issued before Limitation; not necessarily served before limitation. Gujarat High Court in the case of Kanubhai M. Patel HUF vs. Hiren Bhatt 334 ITR 25 (Guj) has held that if notice is not given to post department for service before expiry of limitation period, the same is time barred.

Reopening beyond 3 years – various conditions

6.2. S. 149(1)(a) restricts issuance of notice beyond a period of 3 years from the end of the relevant assessment year unless the case falls under clause (b). S. 149(1)(b) extends the limitation up to 10 years from the end of the relevant assessment year if the AO has in his possession books of account or other documents or evidence which reveal that the income chargeable to tax, represented in the form of asset, expenditure in relation to a transaction or event or occasion or an entry in the books of account giving rise to escapement of income in excess of Rs.50.00 lacs.

Asset criteria

Between 01/04/2021 to 31/03/2022, reopening for extended period beyond 3 years from the end of the relevant assessment year was permissible when escaped income represented in the form of ‘asset’ is revealed from books of accounts or other documents or evidence in possession of AO in excess of Rs.50.00 lacs. ‘Asset’ was defined in an inclusive manner to include immovable property, being land or building or both, shares and securities, loans and advances, deposits in bank account. Resultantly, many transactions involving cash credit, fictitious loss and unaccounted expenditure etc. could not be subjected to reopen as they do not fall within the definition of asset. Legislature having realised this, amended the law to take care of these situations. However, the law is amended prospectively wef 01/04/2022 keeping the old law in force for AY 2021-22.

Is reopening permissible for escaped income not represented in the form of asset, expenditure or entry?

6.3. However, the amended section 149(1)(b) is not happily worded. Even after the amendment, what can trigger reopening under clause (b) would be only that income in excess of Rs.50.00 lacs which is revealed from books of account or other documents or evidence and represented in the form of an asset, expenditure in respect of transaction or in relation to an event or occasion or an entry or entries in the books of account and that has escaped assessment. There are many incomes which may not be represented in the forms as stipulated and hence they may not trigger reopening!. Suppose in a search at builder’s premises, a diary is found out containing details about ‘on money’ for various years far in excess of Rs.50.00 lacs falling within the years contemplated under clause (b). ‘On money’ recorded in a diary would fall within the other documents or evidence in possession of the assessing officer. Diary also reveals income chargeable to tax in the form of ‘on money’. However, what is important is whether such income can be said to be represented in the form of an asset, expenditure, or an entry in the books of account. ‘On money’ is certainly not an asset as asset is defined to mean to include immovable properties, being land or building or both, shares securities, loan and advances and deposits in bank account. ‘On Money’ would not fall under any of these classes of assets nor can it be called in general an asset. It is certainly not an expenditure. Since ‘on money’ is not recorded the books of account, therefore, the same cannot be termed as an entry or entries in the books of account. Therefore, in case of a builder even if evidences are found as regards escapement of income in the form of ‘on money’ charged from the customers, since the same is not represented in the form of an asset, expenditure, or book entry, the same cannot trigger the criteria prescribed under clause (b) to section 149(1) of the Act.

Years where limitation has expired under the old regime cannot be reopened under the new extended time limit

6.4. 1st proviso to S. 149 provides that the years which have already become time barred under the old regime, cannot be reopening due to change in the law and extended limitation period. Originally, when the proviso was introduced reopening under the new regime was not allowed to go back beyond 6 years as contemplated u/s 149(1)(b). However, now S. 153A and S. 153C limitations are also inserted with retrospective effect so the extended limitation of these sections would apply in cases of search taking place after 01/04/2021 and to other appropriate cases where action u/s 153A or 153C could have been taken for a longer period under the old regime.

Search related cases – only ‘asset’ criteria for reopening beyond 6 years

6.5. However, it may not be lost sight of the fact that even under the provisions of section 153A or 153C governing the searches taking place prior to 01.04.2021, reopening of 6th to 10th year prior to the date of search could be possible only if the assessing officer has in his possession the books of account or other documents or evidence which revealed that the income represented in the form of asset in excess of 50,00,000/- or more in any one or in aggregated of more than one Assessment Years has escaped assessment. The definition of asset has remained the same even for the period prior to 01/04/2021. Therefore, even for the searches taking place after 01.04.2021, reopening can take place for the years beyond 6 years only if the escaped income is represented in the form of an asset. The other two criteria as appearing in the existing 149(1)(b) viz. expenditure and book entry cannot be pressed into service for these years as the same were absent under S. 153A and 153C of the Act.

6.6. 2nd proviso states that searches taking places on or before 31/03/2021 would be continued to be governed by S.153A and 153C of the Act and these new provisions would not apply to such cases.

6.7. 3rd proviso is an exclusion clause. While calculating the limitation period as per section 149, the time allowed to respond u/s 148A(b) (7 to 30 days or extended time) is required to be excluded. Also, if the proceedings u/s 148A are stayed by any Court, period of operation of such stay is also to be excluded while calculating the limitation period. S. 149 opens with a negative covenant to the effect that no notice u/s 148 shall be issued beyond the period prescribed u/s 149 unless conditions stipulated u/s 149 are fulfilled. Therefore, this proviso extends the time to issue notice u/s 148 of the Act by the period allowed to the assessee to respond u/s 148A(b) of the Act.

6.8. Section (1A) is newly inserted wef 01/04/2022 which expands the scope of applicability of extended period of limitation under clause (b) of S. 149(1) of the Act. S. 149(1)(b) states that where income chargeable to tax in excess of Rs.50.00 lacs is represented in the form of an asset or expenditure in relation to an event or occasion, then reopening can take place upto 10 years from the end of the relevant assessment year. S. 149(1A) provides that when such sum of Rs.50.00 lacs is incurred in more than one year, all such year or years could be covered in the extended limitation period. Law is silent as regards what is an event or occasion and how the expenditure of Rs.50.00 lacs in relation to such an event or occasion is to be calculated.

7. Section 151: Sanction for issue of notice.

Specified authority for the purposes of section 148A shall be,—

|

(i) |

|

Principal Commissioner or Principal Director or Commissioner or Director, if three years or less than three years have elapsed from the end of the relevant assessment year; |

|

(ii) |

|

Principal Chief Commissioner or Principal Director General or where there is no Principal Chief Commissioner or Principal Director General, Chief Commissioner or Director General, if more than three years have elapsed from the end of the relevant assessment year.] |

7.1. S. 151 defined specified authority referred to in other sections. If reopening is beyond a period of 3 years, sanction of higher authority is contemplated.

8. Section 151A: Faceless assessment of income escaping assessment.

(1) The Central Government may make a scheme, by notification in the Official Gazette, for the purposes of assessment, reassessment or re-computation under section 147 or issuance of notice under section 148 or conducting of enquiries or issuance of show-cause notice or passing of order under section 148A or sanction for issue of such notice under section 151, so as to impart greater efficiency, transparency and accountability by—

|

(a) |

|

eliminating the interface between the income-tax authority and the assessee or any other person to the extent technologically feasible; |

|

(b) |

|

optimising utilisation of the resources through economies of scale and functional specialisation; |

|

(c) |

|

introducing a team-based assessment, reassessment, re-computation or issuance or sanction of notice with dynamic jurisdiction. |

(2) The Central Government may, for the purpose of giving effect to the scheme made under sub-section (1), by notification in the Official Gazette, direct that any of the provisions of this Act shall not apply or shall apply with such exceptions, modifications and adaptations as may be specified in the notification:

Provided that no direction shall be issued after the 31st day of March, 2022.

(3) Every notification issued under sub-section (1) and sub-section (2) shall, as soon as may be after the notification is issued, be laid before each House of Parliament.

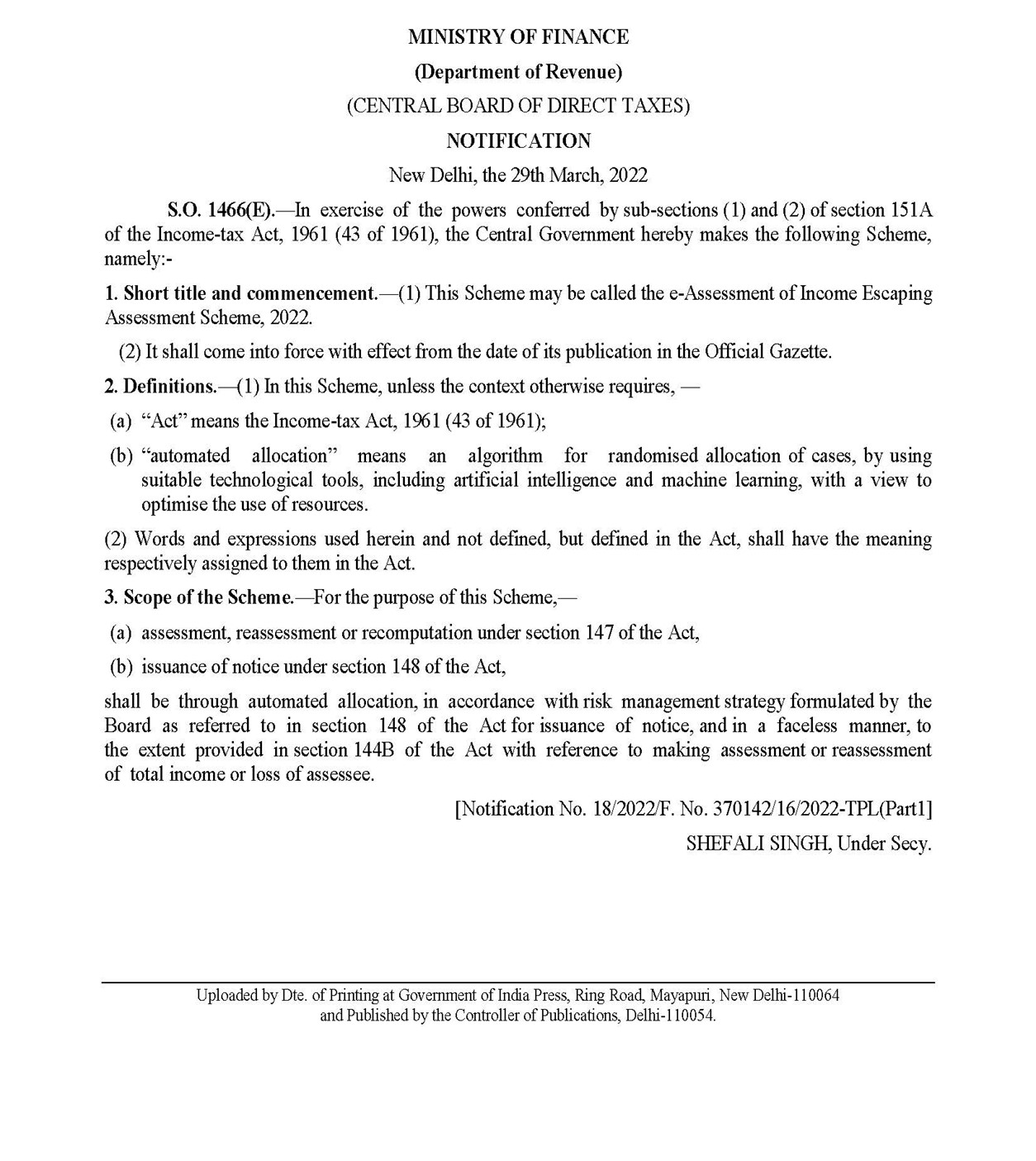

8.1. S. 151A of the Act provides that entire process of reassessment including proceedings u/s 148A and issuance of notice u/s 148 and the entire reassessment proceedings shall be carried out in faceless manner. CBDT has issued Notification No.18/2022 dated 29.03.22 which prescribes scheme for reassessment. The Notification reads:

As per clause (b) of section 3 of the said notification, issuance of notice under section 148 of the Act shall be through automated allocation, in accordance with risk management strategy formulated by the Board as referred to in section 148 of the Act for issuance of notice, and in a faceless manner, to the extent provided in section 144B of the Act with reference to making assessment or reassessment of total income or loss of assessee. Thus, notice under section 148 of the Act has to be issued by the “National Faceless Assessment centre” only. Such notice cannot be issued by “jurisdictional Assessing Officer”. Many cases have come to light where such notices have been issued by the “jurisdictional Assessing Officer” who did not have jurisdiction to issue such notice and therefore, validity of such notices would be questioned.

Pursuant to Hon’ble Supreme Court judgment in the case of Union of India & Ors. Vs Ashish Agarwal (Civil Appeal No.3005/2022 dated 04/05/2022), AO is to supply material and information within a period of 30 days from the date of judgment. However, in view of the Gazette Notification No. 18/2022/F. No. 370142/16/ 2022-TPL (part-I) dated 29-03-2022, it is not clear as to who would be handling these cases: faceless AO or jurisdictional AO?.

Other legal arguments

9. Having analysed the scheme of the new provisions of reopening, I now, propose to discuss some basic principles laid down under the old regime still holding the field and can be pressed into service while challenging the action of reopening under the amended provisions.

9.1. Escapement of Income:

“The result of this exercise would be that even if the expenditure of the so called bogus purchases is disallowed, the only effect it could have is to increase the profit of the assessee which in any case is exempt under section 10AA of the Act. Section 147 of the Act would be applicable where the Assessing Officer has reason to believe that income chargeable to tax has escaped assessment. When this fundamental requirement fails, power of reopening cannot be exercised – Sajani Jewels vs DCIT 241 taxman 383 (Guj).”

9.2. Change of Opinion: Concept of change of opinion is a facet of absence of powers of review under the scheme of the Act. Hon’ble Supreme Court in the case of CIT vs. Kelvinator of India Ltd. [2010] 187 Taxman 312 (SC) explained this as under:

“4. On going through the changes, quoted above, made to section 147 of the Act, we find that, prior to Direct Tax Laws (Amendment) Act, 1987 , re-opening could be done under above two conditions and fulfilment of the said conditions alone conferred jurisdiction on the Assessing Officer to make a back assessment, but in section 147 of the Act [with effect from 1-4-1989], they are given a go-by and only one condition has remained, viz., that where the Assessing Officer has reason to believe that income has escaped assessment, confers jurisdiction to re-open the assessment. Therefore, post 1-4-1989, power to reopen is much wider. However, one needs to give a schematic interpretation to the words "reason to believe" failing which, we are afraid, section 147 would give arbitrary powers to the Assessing Officer to re-open assessments on the basis of "mere change of opinion", which cannot be per se reason to reopen.”

xxx

“We must also keep in mind the conceptual difference between power to review and power to re-assess. The Assessing Officer has no power to review; he has the power to reassess. But reassessment has to be based on fulfillment of certain pre-condition and if the concept of "change of opinion" is removed, as contended on behalf of the Department, then, in the garb of re-opening the assessment, review would take place. One must treat the concept of "change of opinion" as an in-built test to check abuse of power by the Assessing Officer. Hence, after 1-4-1989 , Assessing Officer has power to reopen, provided there is "tangible material" to come to the conclusion that there is escapement of income from assessment. Reasons must have a live link with the formation of the belief. Our view gets support from the changes made to section 147 of the Act, as quoted hereinabove. Under the Direct Tax Laws (Amendment) Act, 1987, Parliament not only deleted the words "reason to believe" but also inserted the word "opinion" in section 147 of the Act. However, on receipt of representations from the Companies against omission of the words "reason to believe", Parliament re-introduced the said expression and deleted the word "opinion" on the ground that it would vest arbitrary powers in the Assessing Officer.”

9.3. Reopening not permissible for roving and/or fishing inquiries:

“For a mere verification of the claim, the power of reopening of assessment could not be exercised. …… Assessing Officer under the guise of power to reopen an assessment, cannot seek to undertake a fishing or roving inquiry and seek to verify the claims, as if it were a scrutiny assessment – Krupesh Ghanshyambhai Thakkar vs DCIT 77 taxmann.com 293 (Guj)

9.4. Live nexus- Cause and Effect relationship between reasons and income escaping assessment: Where Assessing Officer merely mentioned about transaction in notice for reassessment and nothing more and, thus, he had not stated how he had arrived at reason to believe that income had escaped assessment, such notice lacks validity.

10. Reopening under the old regime even after new regime has come into force: