CA Chaitanya Maheshwari and Advocate Ameya Khare have explained the entire law and practice relating to Master File (MF) documentation and Country-by-Country Reporting (CbCR) as are applicable under sections 92D and 286 of the Income-tax Act, 1961 read with the OECD guidelines on ‘Base Erosion and Profit Shifting’ (BEPS)

BEPS Background

The international tax system was born following the First World War, in a climate of financial instability and political uncertainty. It resulted from technical studies in the 1920s and international negotiations in 1928 through the League of Nations.

The project on ‘Base Erosion and Profit Shifting’ (BEPS) has been the first major Global multilateral effort to ameliorate international tax laws since they were first designed in the 1920s. However, the political interests in international taxation first emerged in the 1970s in the context of concerns about the monopoly power and immoral predominance of multinational enterprises, which forced the Organisation for Economic Co-operation and Development (OECD) to invent technical guidance, reports, literature for curbing and preventing the international tax avoidance and evasion practice worldwide.

A new political initiative in the mid-1990s through the G7 countries produced the OECD project on ‘Harmful Tax Competition’. Following the growth of a worldwide tax justice movement, and the famous financial crisis which began in 2007 and lasted till 2009, a more determined and serious stance was taken by the G8 countries and later on the G20 nations. With this impetus in 2014, the OECD gave birth to a new global standard for transparency through comprehensive, multilateral, automatic information exchange for tax and financial purpose came to be known as the Common Reporting Standard (CRS).

The OECD began the project on base erosion and profit shifting (BEPS) in February 2012. In February 2013, at the request of the G20 group of countries, the OECD Published an initial report on its activities in connection with BEPS. The BEPS action plan that followed on from this initial report was issued on 19 July 2013 which contained a combined set of 15 actions to address range of issues including tax transparency, accountability, information exchange and other potential changes to International taxation regime.

The requirements of the template were first published by the OECD in September 2014 followed by implementation guidance in February 2015 and the final implementation package in June 2015. These were all consolidated into the final BEPS report which became universal reality and was published on 5 October 2015. Over 100 countries and jurisdictions are collaborating to implement the BEPS measures and tackle BEPS.

What is MF documentation and CbC reporting?

Master File (MF) documentation and Country-by-Country Reporting (CbCR) is a global transfer pricing (TP) compliance requirement under the transfer pricing laws of countries around the world. It is one of the major amendments in relation to the Indian TP documentation and Global TP compliance pertaining to the Multi National Enterprises (MNEs) Group. This has been introduced vide amendment to section 92D and insertion of new section 286 of the Income-tax Act, 1961 (“the Act”) along with Rules 10DA and 10DB of the Income-tax Rules, 1962 (“the Rules”) (vide Notification No. 92/2017 dated October 31, 2017) effective from the Assessment Year (AY) 2017-18 (i.e. Financial Year 2016-17). This amendment is the consequence of Government of India’s commitment for implementation of the BEPS Action Plan 13 aligning with the Indian TP Legislation. OECD released “Guidance on the implementation of CbC Reporting” and “Guidance on the appropriate use of information contained in CbC Reports” which provides for revised standards for TP documentation and a template for CbCR of income, earnings, taxes paid and certain measure of economic activity. However, the rules and requirements in India are aligned with BEPS action plan 13 with certain modifications w.r.t. guidance issued by OECD. This has further increased the compliance burden for the Constituent Entities (CEs) in India, especially which are part of foreign International Groups (IGs).

Following three-tiered standardised structure has been mandated to enable the tax authorities to have sufficient information to assess risk:

| S. No. | Name of Document | Description |

| (i) | Master File | Containing comprehensive information relevant for all MNE group members (it is an overview of the MNE group’s business, including the nature of its global business operations, its overall TP policies, and its global allocation of income and economic activity) refer Annex II of Chapter V of the Transfer Pricing Guidelines issued by OECD. |

| (ii) | Local File | Which is entity-specific information with reference to the related party transactions of the local taxpayer entity of the MNE (this is mainly the normal TP Study report as per Rule 10D of the Rules); refer Annex I of Chapter V of the Transfer Pricing Guidelines issued by OECD |

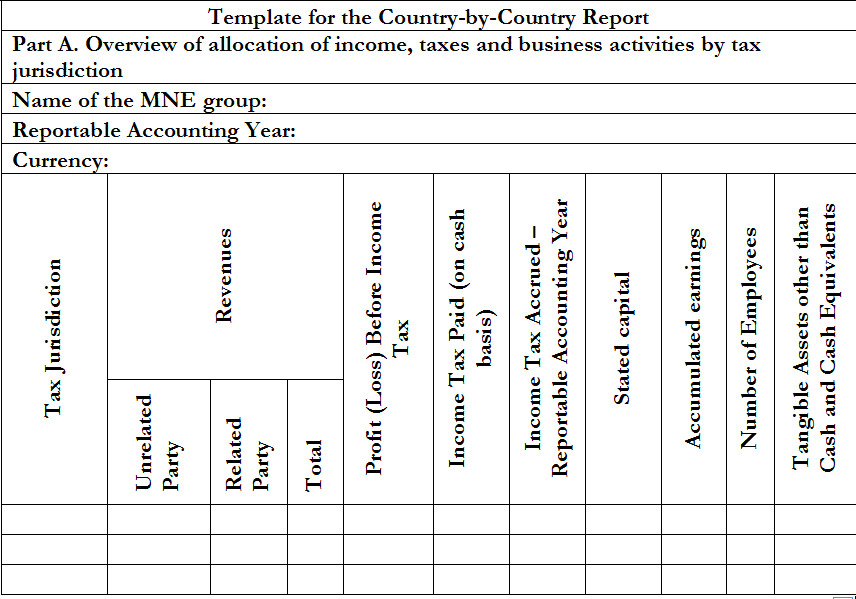

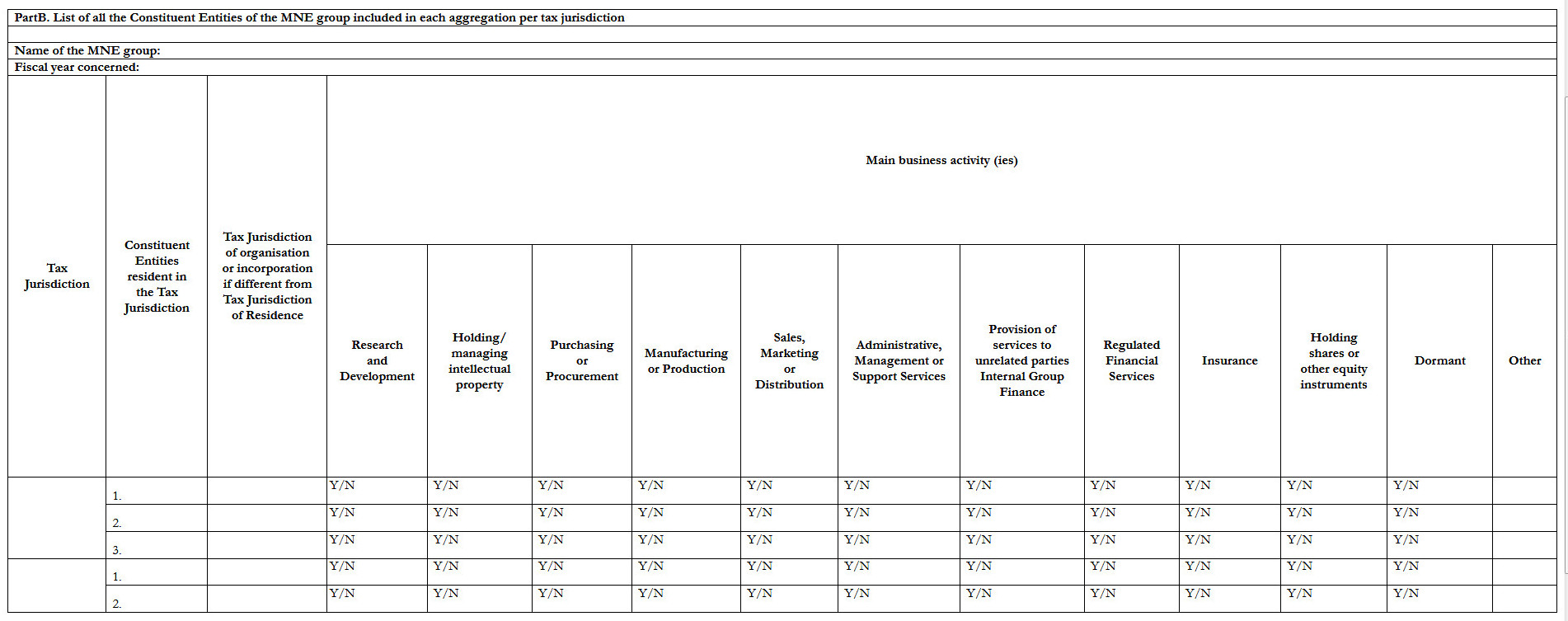

| (iii) | Country-By-Country Report | Consists of certain information relating to the global allocation of the MNE’s income and taxes paid together with certain indicators of economic activity like revenue, taxes paid, capital employed, head count etc. of each entity within the MNE group. Following is the format of such reporting as per OECD User Guide known as "Template for the Country-by-Country Report". |

What are the objectives of MF documentation and CbCR?

The major objectives of the BEPS Action Plan 13 i.e. MF documentation and CbCR are as follows:

a. Aid tax authorities to perform a TP risk assessment;

b. Ensure taxpayers give appropriate consideration to setting prices consistent with the arm’s-length principle;

c. Provide information needed for tax authority audit.

What are the key provisions relating to MF documentation and CbCR under the Indian Income-tax Act?

The MF documentation and CbCR are applicable as per the following provisions of the Indian Income-tax Act:

a. Proviso to Section 92D(1): Casts responsibility of preparation and maintenance of Master File documentation on constituent entity of an international group.

b. Section 92D: Casts responsibility of filing of MF documentation on constituent entity of an international group in the prescribed form (Forms 3CEAA and 3CEAB as per Rule 10DA).

c. Section 286: Preparation, maintenance and filing of CbC Report as per the prescribed forms by the resident holding company or alternate reporting entity and the constituent entity of an international group (Forms 3CEAC, 3CEAD and 3CEAE as per Rule 10DB).

Which types of entities are required to comply with the MF documentation and CbCR in India?

Mainly the said compliance has to done by one of the constituent entity of the international group (IG) if certain prescribed financial limits are exceeded under the relevant provisions of the Act for specified accounting year of the ultimate parent entity of the IG. Since the word “entity” is a broader term so it has to be read to include all types of business units or enterprises as follows:

a. Company,

b. Proprietorship Firm or Individual,

c. LLPs and partnership firms,

d. Any other form of businesses irrelevant of its constitution like AOP, BOI etc.

However, the compliance has to be done only by that constituent entity:

i. which consolidates in its financial statements, financial statements of all other entities of the IG; or

ii. whose financial statements are being consolidated in the financial statements of the ultimate parent entity of the IG.

Moreover, said consolidation is to be seen as per the applicable accounting standards or laws in the tax jurisdiction where the parent entity is resident. In addition, if the equity shares of the entity would have been listed on a stock exchange and as per the rules and regulations consolidation of financial statements needs to be done by the parent entity in its tax jurisdiction, then the constituent entity of that IG needs to comply with MF documentation and CbCR.

What are the conditions for the applicability of various forms?

The following table highlights conditions for applicability of various forms:

| S. No. | Form No. | Conditions for Applicability |

| Master File Documentation | ||

| 1 | 3CEAA – Part A | Any Constituent entity of an international group [Rule 10DA(1) and 10DA(3)(i)] |

| 2 | 3CEAA – Part B | Constituent Entity, if following conditions are satisfied [Rule 10DA(1) and 10DA(3)(ii)]:

|

| 3 | 3CEAB | If more than one constituent entities are resident in India then one of the entities has to be designated by the international group as the designated entity to furnish Form 3CEAA. Such information to be intimated by the designated constituent entity to the Department in Form 3CEAB. |

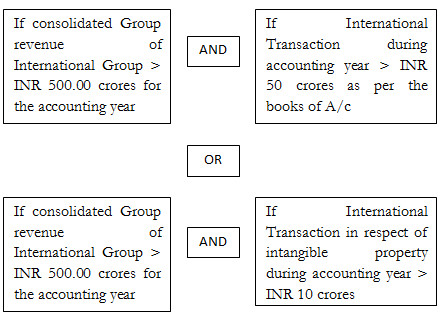

| CbC Documentation to be complied by the international group having total consolidated group revenue > INR 5,500 crores* for accounting year ending on or before March 31, 2016 (for AY 2017-18) [similar ratio applicable to subsequent AY]: | ||

| 4 | 3CEAC | To be filed by constituent entity, if its parent entity is non-resident in India, for intimating whether: (i) the constituent entity is the alternate reporting entity, or; (ii) details of the parent entity or the alternate reporting entity and the countries in which they are residents |

| 5 | 3CEAD | To be filed by the resident parent entity or the alternate reporting entity of the international group resident in India. This is the country-by country reporting template. |

| 6 | 3CEAE | If more than one constituent entities of the either of the following IG are resident in India then one of the entities has to be designated by the IG as the designated entity to furnish Form 3CEAD:

(a) if the parent entity is tax resident of the country or territory with which India does not have agreement for providing exchange of CbCR with India; or (b) the parent entity is tax resident of the country or territory which has suspended or failed to exchange the CbCR with India. Then, such information to be intimated by the designated constituent entity to the Department in Form 3CEAE. |

*As per section 286 (7) r.w.r. 10DA as well as 10DB of the Act, the above compliance is applicable in respect of a MNE group having total consolidated group revenue for the accounting year preceding to the relevant accounting year exceeding the prescribed amount or threshold limit. Currently, the said threshold limit as per the global consensus is € 750 million which is equivalent to INR 5,500 crores [as per Rule 10DB(6) of the Rules]. So for AY 2017-18, the Consolidated Revenue of the Group is required for the Accounting Year of the parent entity ending just before April 01, 2016.

What is meant by International Group?

As per Section 286(9)(g) of the Act, "international group" means any group that includes,—

(i) two or more enterprises which are resident of different countries or territories; or

(ii) an enterprise, being a resident of one country or territory, which carries on any business through a permanent establishment in other countries or territories;

In addition to this, as per Section 286(9)(e) of the Act, "group" includes a parent entity and all the entities in respect of which, for the reason of ownership or control, a consolidated financial statement for financial reporting purposes,—

(i) is required to be prepared under any law for the time being in force or the accounting standards of the country or territory of which the parent entity is resident; or

(ii) would have been required to be prepared had the equity shares of any of the enterprises were listed on a stock exchange in the country or territory of which the parent entity is resident.

From the above definition we can say that:

a. An entity resident in India say X Ltd. having subsidiary in USA say Y Inc., then they both collectively would constitute an international group. X Ltd. Is required to prepare consolidated financial statements as per Indian Accounting Standards.

b. Now, in example in point (a) suppose X Inc. is resident of USA and having a branch Y in India. Then as Y becomes Permanent Establishment (PE) of X Inc., both of them collectively would constitute an international group. As per laws applicable in India the branch Y of X Inc. is required to prepare separate financial statements for operations undertaken by it in India and X Inc. consolidates the same within its financial statements.

In both the above examples, as there are two enterprises which are resident in two different countries, hence they would collectively constitute as a Group u/s 286(9)(e) and further as an International Group u/s 286(9)(g).However, the term enterprise has been defined u/s 92F and not been defined u/s 286 of the Act or has also not been specifically given reference of Section 92F unlike term PE.

The rate of exchange for the calculation of the value in rupees of the consolidated group revenue in foreign currency shall be the telegraphic transfer buying rate of such currency on the last day of the accounting year. The “telegraphic transfer buying rate" shall have the same meaning as assigned in the Explanation to Rule 26 of the Indian Income-tax Rules, 1962.

How to determine Parent Entity of International Group?

As per Section 286(9)(h) of the Act, "parent entity" means a constituent entity, of an international group holding, directly or indirectly, an interest in one or more of the other constituent entities of the international group, such that:

(i)it is required to prepare a consolidated financial statement under any law for the time being in force or the accounting standards of the country or territory of which the entity is resident; or

(ii)it would have been required to prepare a consolidated financial statement had the equity shares of any of the enterprises were listed on a stock exchange,

and, there is no other constituent entity of such group which, due to ownership of any interest, directly or indirectly, in the first mentioned constituent entity, is required to prepare a consolidated financial statement, under the circumstances referred to in sub-clause (i) or sub-clause (ii), that includes the separate financial statement of the first mentioned constituent entity.

From the above definition we can conclude that the parent entity is that entity, say X Ltd., of the international group who ultimately consolidates financial statements of all other group entities as per the applicable laws or accounting standards in the country or territory in which X Ltd. is resident; or the liability on X Ltd. to prepare consolidated financial statements arises as if it would have been listed on a stock exchange; and there is no group entity which consolidates financial statements of the first mentioned group entity i.e. X Ltd. in its financial statements. But if suppose there is group entity Y Ltd. which consolidates financial statements of X Ltd. in its books, then Y Ltd. would be the parent entity and not X Ltd.

Whether for computing Total Consolidated Group Revenues per Rule 10DB(6) of the Rules extraordinary income and gain from investment activities be included? Also, for reporting purposes in CbC report i.e. Form 3CEAD – Part A in the column "Revenues" this amount to be included?

As per the “Guidance on the Implementation of Country-By-Country Reporting: BEPS Action 13” issued by OECD in determining whether the total consolidated group revenue of an MNE Group is less than INR 5,500 crores for the accounting year ending on or before March 31, 2016, all of the revenue that is (or would be) reflected in the consolidated financial statements should be used. A jurisdiction where the Ultimate Parent Entity (UPE) resides is required to include the extraordinary income and gains from investment activities in total consolidated group revenue if those items are presented in the consolidated financial statements under applicable accounting rules in the country or territory of the UPE.

In addition to above, for the financial entities, which may not record gross amounts from transactions in their financial statements with respect to certain items like interest rate swap etc., the item(s) considered similar to revenue under the applicable accounting rules should be used in the context of financial activities, i.e. here the term ‘revenue’ would mean the net amount from the transaction of interest rate swap. Such items could be labeled as ‘net banking product’, ‘net revenues’ or others depending on accounting rules.

As per the “Guidance on the Implementation of Country-By-Country Reporting: BEPS Action 13” the extraordinary income and gains from investment activities are to be included in "Revenues" column of the CbC Report i.e. Form 3CEAD.

Whether for the purposes of evaluating limits under Rule 10DA(1), can the accounting year be different than previous year?

As per Section 286(9)(a) of the Act, “Accounting Year” has been defined as:

a. In case parent entity or alternate reporting entity is resident in India, the previous year;

b. In case the parent entity of the international group is resident of territory other than India, the accounting year w.r.t. which it prepares its financial statements as per the applicable laws or accounting standards in the country or territory in which it is resident.

From the above definition we can conclude that, in case the parent entity of the international group is not resident in India and if the accounting year as per the applicable laws or accounting standards in the country or territory where the parent entity is resident is different from the previous year in India, then there would be different accounting year than the previous year. For example, if Parent Entity say X Inc. resident in USA and follows calendar year as accounting year then it will be different from the previous year followed by its subsidiary Z India Pvt. Ltd. resident in India.

What are the major reporting requirements of the MF documentation?

Major reporting requirements of the Master File documentation (i.e. Form 3CEAA) as per various categories are as follows:

A. Organisational Structure

1. List of all entities of the international group along with their addresses

2. Chart depicting the legal status of the constituent entity and ownership structure of the entire international group

B. Business Description

1. the nature of the business or businesses

2. important drivers of profits of such business or businesses

3. description of the supply chain for the 5 largest products or services of the international group in terms of revenue and any other products including services amounting to more than 5% of consolidated group revenue;

4. a list and brief description of important service arrangements made among members of the international group, other than those for research and development services

5. a description of the capabilities of the main service providers within the international group

6. details about the transfer pricing policies for allocating service costs and determining prices to be paid for intra-group services

7. a list and description of the major geographical markets (country wise) for the products and services offered by the international group

8. a description of the functions performed, assets employed and risks assumed by the constituent entities of the international group that contribute at least 10% of the –

• revenues or

• assets or

• profits of such group

9. a description of the important business restructuring transactions, acquisitions and divestments

C. Intangibles

1. a description of the overall strategy of the international group for the development, ownership and exploitation of intangible property, including location of principal R&D facilities and their management

2. a list of all entities of the international group engaged in development and management of intangible property along with their addresses

3. a list of all the important intangible property or groups of intangible property owned by the international group along with the names and addresses of the group entities that legally own such intangible property

4. a list and brief description of important agreements among members of the international group related to intangible property, including cost contribution arrangements, principal research service agreements and license agreements

5. a detailed description of the transfer pricing policies of the international group related to R&D and intangible property

6. a description of important transfers of interest in intangible property, if any, among entities of the international group, including the name and address of the selling and buying entities and the compensation paid for such transfers

D. Financial Activities

1. a detailed description of the financing arrangements of the international group, including the names and addresses of the top ten unrelated lenders

2. a list of group entities that provide central financing functions, including their place (addresses) of operation and of effective management (POEM)

3. a detailed description of the transfer pricing policies of the international group related to financing arrangements among group entities

E. Financial and Tax Position

1. a copy of the annual CFS of the international group

2. a list and brief description of the existing unilateral advance pricing agreements and other tax rulings in respect of the international group for allocation of income among countries

Note: The Master File shall be kept and maintained for a period of 8 years from the end of relevant assessment year (the year following the tax year).

What are the major reporting requirements of the CbC documentation (i.e. Form 3CEAD)?

Following is the CbC reporting templates which also shows the information and requirements to be reported in Form 3CEAD:

From which year does MF documentation and CbCR required to be complied in India?

The said TP compliance is applicable from AY 2017-18 and onwards. The due dates of e-filing of various forms as per Rules 10DA and 10DB of the Rules are as under:

| S. No. | Documentation | Form No. | Due Date for AY 2017-18 | Due Date for subsequent AYs |

| 1 | Master File | Form 3CEAA – Part A | March 31, 2018 | Due date of filing return of income |

| 2 | Form 3CEAA – Part B | March 31, 2018 | Due date of filing return of income | |

| 3 | Form 3CEAB | March 01, 2018 | 30 days before the due date for filing Form No. 3CEAA | |

| 4 | CbC | Form 3CEAC | January 31, 2018 | 2 months prior to due date for filing Form No. 3CEAD |

| 5 | Form 3CEAD | March 31, 2018 | Due date of filing return of income | |

| 6 | Form 3CEAE | Yet to be clarified by CBDT | Yet to be clarified by CBDT |

Whether any penalty on non-compliance?

Non-compliance of the same will attract severe monetary penalty under the provisions of the Act as follows:

| S. No. | Penalty Section | Description of the Penalty Provision | Quantum of Penalty (INR) |

| 1 | 271AA(2) | Failure to furnish Master File documentation prescribed u/s 92D(4) | 5,00,000 |

| 2 | 271GB(1) | Failure to furnish CbC Report (Form 3CEAD) | i) 5,000 per day if failure continues till 1 month ii) 15,000 per day if failure continues beyond 1 month |

| 3 | 271GB(2) | Furnishing of information and documentation as per Notice issued by the prescribed authority | 5,000 per day from day of expiration on which period of furnishing the information and documentation expires |

| 4 | 271GB(3) | If Penalty order issued by the prescribed authority for 271GB(1) and 271GB(2) | 50,000 per day from the date of service of such order |

| 5 | 271GB(4) | Inaccurate particulars are been furnished and:

i) entity has knowledge of inaccuracy at time of furnishing the report; or ii) entity discovers inaccuracy after furnishing the report and fails to inform and furnish correct report within 15 days of such discovery; or iii) entity furnishes inaccurate information or document in response to notice issued u/s 286(6) |

5,00,000 |

What are the key differences between OECD requirements vis-a-via requirements under the CBDT final rules in India?

The following table is a snapshot of additional documentation requirement in India compared to OECD requirements:

| Master File Requirement | OECD BEPS Action 13 Requirements | CBDT Notified IT Rules Requirements |

| Organization structure |

|

|

| Description of business |

|

|

| Intangibles |

|

|

| Intercompany financial activities |

|

|

What are the major challenges in compliance of MF documentation and CbCR?

The major challenges ahead:

- Identifying the Parent Entity and Constituent Entity (CE) of international group;

- Collection of data from entities across the globe is a time consuming activity;

- Authenticity of data provided by CEs, especially those not included in CFS –the data furnished may be unaudited;

- The data may be highly confidential and prone to cyber theft;

- Aligning of the enormous data in a particular format;

- Interpretation of statutory provisions;

- Risk assessment exercise of the data to be submitted;

- Utility for electronic forms yet to be uploaded on e-filing website;

- System challenges in e-filing of various forms;

- Increase in litigations in absence of clarity of law; etc.

Conclusion

The unprecedented attention to aggressive international tax planning has shaken the earth under the most powerful players in the world of international tax administration and policy design. The emerging economies particularly India, China and Brazil have taken a more active role in the shaping of the new fangled international tax regime, despite not being OECD members. The Indian Courts and Judiciary discover and interprets tax laws delivers judgments which today in the current trend the world watches using binocular vision.

The CBDT’s final rules on MF and CbCR seek more data than OECD. The CBDT is marching a step ahead by ordering on the table information beyond the menu of BEPS Action 13. Considering more detailed requirements of the CBDT‘s final rules in comparison to the OECD requirements it gives a clear impression and looks that the CBDT is claiming itself to become the New OECD.

Even though CBDT has notified the Rules and respective Forms thereby in relation to MF documentation and CbCR on October 31, 2017, the said Forms are yet to be uploaded on the Income-tax website in electronic format. To our surprise, the CBDT once uploaded Forms 3CEAA and 3CEAD (screenshots of which are attached with this article in excel files) on December 14, 2017 at its e-filing website, the same have been withdrawn by CBDT from the website within very short period (say 4-5 days). Such surprising activity has been rarely done in past by CBDT. We would further like to bring to the notice of everyone that the due dates of the Forms are not far away and very short period of time is left to e-file them.

However, the Government of India (GOI) is fully committed and taking strategic steps to increase transparency and ease of doing business in India in sync with global standards. With introduction of key legislations, policies, reforms taking place such as GST, Ind AS in line with IFRS, RERA, IBC regulations, India marched ahead to form part of top 100 countries on World Bank’s ‘Ease of Doing Business’ rankings. India in 2017 tramped towards bringing its tax laws in harmony with the BEPS agenda. At the present moment the GOI is on a crucial mission towards transforming India to Developed India and is positively moving in full force towards achieving its dream of India Vision 2020.

Wish you all a Happy and Prosperous New Year 2018 amid the era of compliances.

| Disclaimer: The contents of this document are solely for informational purpose. It does not constitute professional advice or a formal recommendation. While due care has been taken in preparing this document, the existence of mistakes and omissions herein is not ruled out. Neither the author nor itatonline.org and its affiliates accepts any liabilities for any loss or damage of any kind arising out of any inaccurate or incomplete information in this document nor for any actions taken in reliance thereon. No part of this document should be distributed or copied (except for personal, non-commercial use) without express written permission of itatonline.org |

1) In case of a Firm / Individuals, wherein statute does not provide for consolidated financial statements, will CBCR and Master File be applicable?

2) In case of a joint venture (50:50), the parent will consolidate based on its respective shareholding. What about the Indian constituent entity, which entity is it suppose to identify as its parent for filing Form 3CEAC (since both the companies will be be having equal holding in the Indian constituent entity.

Dear Rushkar,

Our opinions on the queries raised by you above:

1) In case of a Firm/ Individuals, wherein statute does not provide for consolidated financial statements, will CbCR and Master File be applicable?

Ans.) As no statute strictly provide for consolidated financial statements in case of individuals or proprietorship firms. But with reference to Section 286 of the Income Tax Act, 1961 (“the Act”) where on interpreting the definitions of “constituent entity” and “international group” we can make out an example for examples where there can be applicability of CbCR and MFD on entity is operated by individual or proprietorship firm (“the entity”):

a. the entity resident in India having a Branch (a PE) outside India;

b. the entity resident outside India having a Branch (a PE) in India.

In above examples the entity would be considered as International Group as well as its Indian arm would be considered as constituent entity u/s 286.

Hence going as per the wordings of the statute the interpretation of definition of “entity” and “group” appears to be inclusive definition having wider scope.

2) In case of a joint venture (50:50), the parent will consolidate based on its respective shareholding. What about the Indian constituent entity, which entity is it suppose to identify as its parent for filing Form 3CEAC (since both the companies will be be having equal holding in the Indian constituent entity).

Ans.) In the given case, as both the companies are having equal holding in the Indian constituent entity, in our opinion both of them should be mentioned in Form 3CEAC (when CbCR applicable to both the groups which entered into JV), even though the Income Tax Act, 1961 has not given clear cut formula for the purpose of identifying the parent in case of a joint venture (50:50) for filing Form 3CEAC.

On the other hand, one stand can also be taken, since the statue is silent the assessee may be given a privilege for designating the parent entity of his choice for the propose of reporting of international group. But this stand can be argued by the Department.

[CA Chaitanya Maheshwari (Mob:+91 9930511578 and e-mail: cachaitanyamaheshwari@live.com) and Adv. Ameya Khare(Mob: +91 9820420476 and e-mail: ameya.khare@yahoo.com)]