STANDARD OPERATING PROCEDURE (SOP) TO HANDLE CASES OF BOGUS LONG TERM CAPITAL GAIN/LOSS MAINLY PENNY STOCK

SOP to handle cases of penny stock

In last two years, in many cases information has been received from various DIT(Investigation) wings mainly Kolkata, Delhi, Ahmedabad about bogus long term capital gain/loss commonly termed as penny stock. Many of such cases has been re-opened, many such cases are in pipe line of re-opening, in many cases information has also been supplied in ITD system itself through AIMS (Actionable Information Module System). With all these cases, detailed voluminous report is circulated along with data necessary for finalizing the assessment. It is also important to point out that numbers of such penny scrips are huge, and although till now department is able to find more than 95 such scrips, but still there are many other such scrips have been remain out of investigation. Thus, it is important for AO, not only to follow the investigation in cases where information has been received, but also to see all the cases of LTCG/LTCL from the point of view of identifying the new bogus penny stock/scrips, by following the method provided herein.

3. How this all started:

In Finance Act, 2004, Government of India has introduced the Security Transaction Tax (STT) both at the time of purchase and sale, irrespective of profit or loss emanating from transaction, as a measure to avoid the capital gain tax. As a natural corollary to same, STCG emanating from share transaction was revised from 30% to 10% (which was later on revised to 15% by Finance Act, 2008) and LTCG was made exempt by introduction of section 10(38). However, this wise move on part of department, later on become, a major route for tax evasion, as a syndicate of Operator, broker & scrip promoters, came together and started to use this method for providing bogus long term capital gain/loss.

4. Modus Operandi:

Modus Operandi of entire bogus LTCG/LTCL can be summarized as below:

4.1 Becoming of Scrip Operator: The most important person in this entire scam is Scrip Operator. This is person, who manages the overall scheme of the scam. An operator maintains a complex nexus of various paper/bogus entities and is also in control of some companies whose shares are listed on one or the other Stock Exchanges. He maintains a close nexus with share brokers.

A. Any person desirous of becoming Scrip Operator need to have control over various paper/bogus entities including companies/firms/ proprietorship concerns popularly known as Jama-Kharchi entities. Thus the Entry Operators, dealing in providing the bogus share capital/loan/cheque discounting are naturally the person who become

SOP to handle cases of penny stock Scrip Operator, as they already has a plethora of Jama-kharchi entities with them.

B. Jama-Kharchi entities, are generally held in the name of various person either Operators own employees or any other person, who are of no means and are ready to give their name, signature, PAN card etc for a sum as small as Rs. 2000/- to 10000/-. Proprietorship concerns are generally used to deposit the cash and then transferring the same to other entities operated by same operator. These proprietorship concerns either do not file their return of income, or even when filed majority time the bank accounts were not accounted while filing their ROI. These bank accounts typically function only for very small time to avoid investigation by any authority. Normally the companies and firm involved in syndicate do file their return of income by showing literally nil or meager income, do have the audit report; however, if intelligent way is applied in analyzing the bank account of these entities & profit and loss accounts and balance sheet of these entities, it is not difficult to prove that transaction shown in bank accounts have not been taken in account while preparing the financial statements.

C. When any entry operator wishes to become scrip operator and want to start the business of giving bogus LTCG/LTCL, first and foremost task is to control all the shares of a listed scrip.

For this purpose Operator on his own or with the financial support of intermediary agent purchases a company listed on BSE and having a small capital base(company is purchased by transferring all the shares in name of themselves or in name of bogus entities/persons controlled and managed by them).

The basic criterion for purchase of a company is a small capital base with all of shareholding with the promoters and with their dummy persons. As listed companies must have some equity held by public (other than promoters) only persons of dubious reputation and unfair means can control 100% shares of company by using the dummy persons.

Many a times, entry operators also managed to list their own bogus Jama Kharchi Company in some stock exchange by bringing out IPO, which is subscribed fully by their own controlled jama-kharchi entities, for this purpose many a time, operator merges its own jama-kharchis companies for creating high bogus base.

Sometime, when an aspirant scrip operator is not able to purchase a listed company or unable to get its own company listed, because of financial crunch, they get in connivance with promoters/directors of a penny stock company, a company having small capital base and 100% shares are in control of promoter either in their name or through their dummy person, who in turn allow the operator to manage each and every share of their company for some brokerage/commission and benefit of high share price for sometime, which can be used for taking the loans from Bank etc.

D. Out of above three methods of controlling the listed company namely (i) purchase/acquisition of already listed company; (ii) getting listed their own company; (iii) controlling shares of listed company in connivance with promoters; in first two cases atleast that listed company is just a paper entity devoid of any actual financial standing, which can be seen from analysis of financial statements of company having literally no/meager income or many a times even no/meager turnover; and no actual worth/assets although the balance sheet of company may look fat having huge capital and reserve surplus which is created by circular subscription of shares thus increasing the capital and reserve & surplus by equivalent increase in bogus investments in bogus jama-kharchi companies.

E. Once Operator get control over 100% shares of any listed company by any of the three ways mentioned in (D), he is ready to become a Scrip Operator.

F. The last requirement for becoming Scrip operator is having connivance with Share brokers, who allow operator to open Demat accounts and do the trades in name of bogus entities (jama-kharchi Companies) by flouting the KYC norms, escaping the back ground check as required by SEBI. Many a times brokers do the required transactions in name of bogus entities themselves.

In nutshell becoming a scrip operator person need to have control over shares of Scrip either by owning the listed company or in connivance with promoters of some listed company, control and manages huge numbers of bogus entities to launder the cash and movement of scrip, and finally to be hand in gloves with share broker who allow them to trade or trade on behalf of them through bogus entities by flouting the KYC norms and escaping the background check.

4.2 Providing the Bogus LTCG:

Entire process can be understood as under:

I. Let us suppose that there is a person “B” (Beneficiary) who is in possession of unaccounted money and who wants to bring this unaccounted money into his books. At the same time this person also desires to avoid paying any tax whatsoever when this money is brought into the books.

II. Now this person “B” approaches the Scrip Operators “O” either directly or through some sub-broker who may be another entry operator/CA/share broker, who in turn tells B to go for bogus LTCG, as it is tax free u/s 138.

III. Once deal is finalized regarding the quantum and commission, O arranges “B” to buy some specific number of shares of a specific listed company. At this time shares of that listed company are available at very low price, many a time, much below even the par value. These shares can be bought by the Beneficiary in one of the following ways :

a. B buy shares on the exchange itself in a pre-arrangement by telling specific time and numbers to ordered (so that at same time, Operator releases shares from one of the entity in which he held those shares).

b. Or Operator gives details of one of his broker, who do that transaction on behalf of B. Or

c. If needed Operator may arrange for the issue of these shares to the beneficiary through preferential allotment i.e. through private placement (this is an off-market transaction), which has one year lock-in. In such cases there is strong possibility that B purchases these shares at par value or at some premium (depending upon book value of share) which may be much high than being the price of that share on BSE/CSE etc.

d. Many a time Operator O arranges to allot B, shares in some private limited company, which in turn get merged with listed company and B get shares of listed company. In such cases by arranging the swap ratio in such a way that effective cost of share in hand of B become very low, despite the fact that shares of that listed company already are at high level. It can be understood by following example:

Listed company trading at 250/- per share (having book value of Rs. 10/- per share)

Unlisted companies allotted shares at a premium of 240/- per share thereby the increasing the book value of Rs. 250/- per share.

As the most adopted way to determine the swap ratio is ratio of book value; swap ratio will be 1:25 i.e. holder of one share of unlisted company will get 25 shares of listed company according to scheme of amalgamation.

Thus the cost of share in hand of B wd be Rs.10/-, despite being traded at Rs.250/-. This method is mainly useful to give entry to B, when share prices has already been jacked up.

e. Many a times B approaches O, at last hour, when he donot have time to wait for one year for getting the entry. In such cases, B is allot shares by backdating the off market transaction, which can be visible from the fact date of dematerialization of shares in account of B in very near to sell of shares, and no payment for purchase of shares is done through cheque or done at much later date.

f. In this leg of purchase of shares, most of time, B gets his money back in cash from O after deducting a security amount. So B does not have any risk involve.

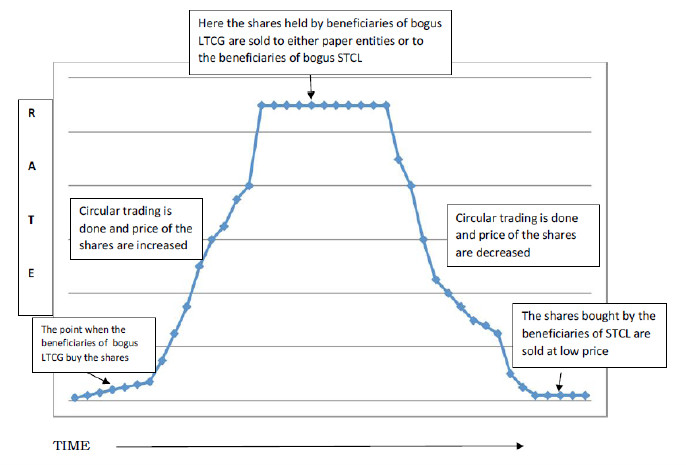

IV. Thereafter, the Operator starts rigging the price of the shares through circular trading and increases the price of the shares, with the help of share brokers and bogus clients. The prices are rigged to an optimum amount over a period of time.

The trading volume of shares during the period, in which manipulations are done to raise the market price, is extremely thin. If an analysis if this period is done, it became clear that only few of entities all bogus paper entities operated by O are involved in trading in this period.

V. In this period to avoid the eye of SEBI, many a times issuing of bonus shares, splitting of shares, frequent change in name and address of listed company is done.

VI. Once a period of 1 year (for claim of exemption on LTCG u/s 10 (38)) is over, the operator asks the beneficiary to deliver the unaccounted cash.

Once the unaccounted cash has been delivered by the beneficiary, the same is then routed by the operator to the books of various Paper/Bogus Companies which ultimately buy the shares belonging to the beneficiary at high prices.

The cash is routed to the books of bogus companies through a maze of various other paper companies so as to avoid the direct cash trail. Normally cash is deposited in proprietorship concerns, which donot file any ROI, and than layered between various paper entities.

Once the cash has been routed to the books of paper/bogus companies, which are registered as clients to the brokers, the operator instructs the Beneficiary to place a sell option for the shares belonging to the beneficiary, in a particular lot size on a particular date and time.

At the same time the operator instructs the paper/bogus companies maintained by him to buy the shares of the beneficiary on the exchange at the predetermined particular date and time. In this way the shares of the beneficiaries are bought by the paper/bogus companies and the unaccounted money of the beneficiary is routed to the books of the beneficiary as a bogus entry of LTCG.

4.3. BOGUS SHORT TERM CAPITAL LOSS

Sometimes, the operator also has request from some companies which foresee that they are going to have huge profits in their books of accounts. The Company wishes to reduce its taxable income by taking entry of bogus loss in its books of account so as to set-off the profit that it is going to earn. These companies are given entry of bogus Short term Capital Loss in the following manner:

I. Let us suppose that there is a person “C” (Beneficiary) which foresees that it is going to have huge profits in its books of accounts. The Company wishes to reduce its taxable income by taking entry of bogus loss in its books of account so as to set-off the profit that it is going to earn.

II. Now this person “B” approaches the Scrip Operators “O” either directly or through some sub-broker who may be another entry operator/CA/share broker, who in turn tells B to go for bogus STCL, to setoff its already crystallized income.

III. When approached by “B”, the operator asks the “B” to buy some specific number of shares of a specific listed company. These shares are bought by the beneficiary company at very high price on the stock exchange.

The shares which are bought by the beneficiary company are held by either the paper/bogus entities maintained by the operator or by the beneficiaries B (who wish to take an entry of bogus LTCG in their books as discussed in para 4.2).

Many a time this transaction is also done offline to save the STT and even to backdate the transaction.

IV. Thereafter, the Operator riggs the price of the shares through circular trading and decreases the price of the scrip. The prices are rigged to an optimum amount over a period of time. Again this time, volumes are thin and narrow and done only by limited entities controlled by Operator.

V. Once the price of the shares has been decreased by circular trading, the operator asks the beneficiary company to place a sell option for the shares belonging to the beneficiary in a particular lot size on a particular date and time, which is than purchased by bogus entities operated by O.

VI. The loss that is incurred by the Beneficiary company is returned back to the company in cash.

VII. In this way the beneficiary companies desirous of booking a loss in their books of account get an entry of bogus STCL which is set-off against the regular profit of the company.

4.4 Summary of modus operandi: Entire modus Operandi can be summarized through following chart & flow diagram.

On the basis of above, the entities involved in this scheme of price manipulation of shares and entry of bogus LTCG and bogus STCL are as follows:

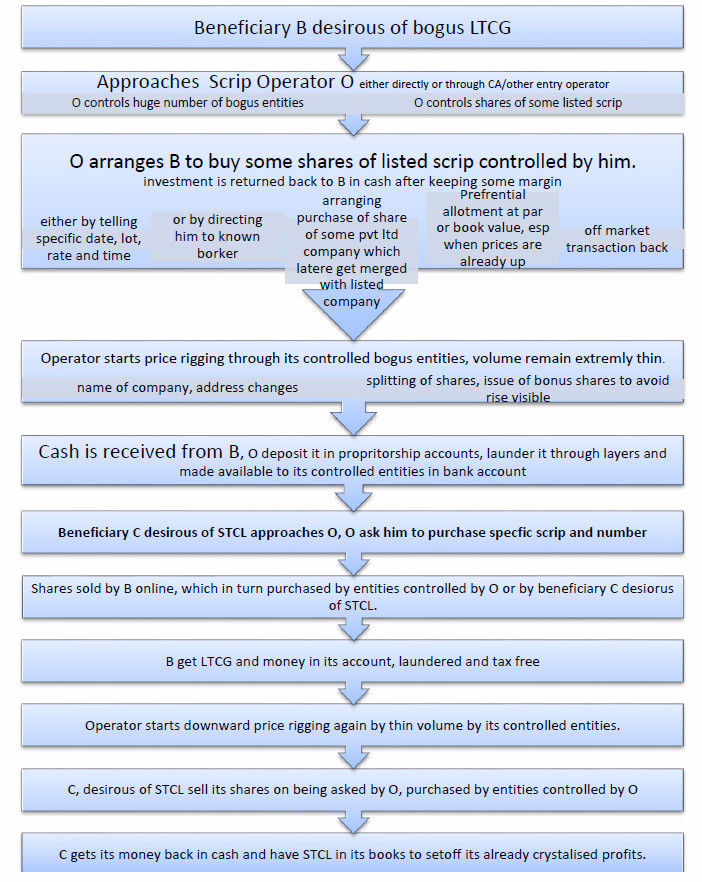

(i) Beneficiary B desirous of bogus LTCG

(ii) Approaches Scrip Operator O either directly or through CA/other entry operator

O controls huge number of bogus entities

O controls shares of some listed scrip

(iii) O arranges B to buy some shares of listed scrip controlled by him. investment is returned back to B in cash after keeping some margin

either by telling specific date, lot, rate and time

or by directing him to known borker

arranging purchase of share of some pvt ltd company which latere get merged with listed company

Prefrential allotment at par or book value, esp when prices are already up

off market transaction back

(iv) Operator starts price rigging through its controlled bogus entities, volume remain extremly thin.

name of company, address changes

splitting of shares, issue of bonus shares to avoid rise visible

(v) Cash is received from B, O deposit it in propritorship accounts, launder it through layers and made available to its controlled entities in bank account

(vi) Beneficiary C desirous of STCL approaches O, O ask him to purchase specfic scrip and number

(vii) Shares sold by B online, which in turn purchased by entities controlled by O or by beneficiary C desiorus of STCL.

(viii) B get LTCG and money in its account, laundered and tax free

(ix) Operator starts downward price rigging again by thin volume by its controlled entities.

(x) C, desirous of STCL sell its shares on being asked by O, purchased by entities controlled by O

(xi) C gets its money back in cash and have STCL in its books to setoff its already crystalised profits.

a. The operator of the Scrip known as O.

b. Directors/promoters of the listed stock (Penny Stock Companies) whose price are manipulated, which many a time many be Operator or its associate.

c. The beneficiaries of LTCG B.

d. The beneficiaries of STCL C.

e. Bogus/paper entities maintained by the operator which are involved in price manipulation and in providing exit to the beneficiaries from the exchange.

f. The share brokers who provide the access of stock market to these bogus/paper entities, in lieu of high brokerage and cash commissions.

5. Action Point for A.O.:

5.1 What need to be proved in cases of LTCG/LTCL/STCL:

Based on understanding of issue in brief in above paras, mainly para 4, we can summarize the issues in hand to be proved by A.O.

Assessee purchased shares of a company/scrip which is devoid of any basic fundamentals.

Listed company does not have any business as seen from its last many P&L accounts and donot have any fixed assets or plant and machinery (most of assets are either investment or loans and advances, it is best to prove that these investments/loans/advances are also in bogus entities).

In some cases listed company may have some business and some fixed assets too, in those cases it has to be proved that same were insufficient for justifying investment by assessee and price movement, by taking comparable cases from known big group companies in that line of business.

The price movement of Scrip is Bell shaped, that means huge rise and price over a short span of time and then sharp decline in price of share. And not matching with overall movement of share market in general and movement of other scrips in same line of business.

Price movement of scrip upward and down word done mainly through thin volume and all/most entities involved in the same are related in some way and are mainly operated by some entry operator and are bogus.

Transactions of assessee in particular both purchase and sell are on other hand are effected by bogus entities controlled by some entry operator.

Brokers have failed to maintain the stringent KYC norms and background check in case of entities involved in price movement.

Statement of entities involved in price movement, entities on other hand of purchase/sale transaction of assessee, scrip operator, promoters of listed company and broker; either accepting their role in giving bogus entries or pushing them at the edge wherein it can be said that these statements are not acceptable.

Statement of assessee, either accepting the entry or pushing to edge that transactions cannot be termed to be carried out in sound financial way.

A backward probe in bank account of entities at other end of assessee’s purchase and sale to reveal either cash deposit or cash withdrawal.

Any order from SEBI/BSE/NSE regarding the scrip wherein genuiness of price movement is doubted.

Any other reference case where any other person accepted similar transactions as bogus.

It is important to mention here, that in many cases all of these points may not be proved fully, but order proving even part of these would be sufficient to make a good case.

5.2 Identifying the bogus LTCG/STCL/LTCL: First and foremost task before A.O. is to identify bogus LTCG/STCL/LTCL. The cases which have been re-opened, or are in scrutiny on the basis of information available this task is already done.

However, this task is first and foremost task before A.O. even in those cases, as this data later-on would be used for finalizing the assessment order too, and in cases where no such information is available, AO need to apply following tests to either reach at a conclusion that LTCG/LTCL/STCL is genuine or may be a case of bogus LTCG/LTCL/STCL. On the basis of discussion in para 4, following are the features of bogus LTCG/LTCL/STCL which can be seen by AO from the basic details given by assessee and small homework on internet:

A. Any person shows huge amount of LTCG/STCL/LTCL, much more than his regular income from all other sources in case of LTCG and STCL/LTCL matching with extra-ordinary income (income higher than normally shown by assessee in earlier years) earned yielding lower tax.

B. Most of LTCG/STCL/LTCL is resulting only from few scrips, in most cases one or two.

C. LTCG is many times the purchase value, and LTCL/STCL is many time the sale value i.e. huge fluctuation in rate of scrip over small period, much more than nation average of BSE/NSE.

D. Typical holding period shown is just more than one year in case of LTCG and LTCL and just few months (anything less than one year) in STCL, generally matching with period of crystallization of extra ordinary income.

The above four parameters are sufficient to identify the bogus LTCG/STCL/LTCL, than the work basically proving the same remain.

5.2 Gathering the information available in public domain: In today’s word so much information is available online, if used effectively gives great insight to assessing officer and also held in making a better case.

A. Type the name of scrip in google, u would get many sites. Please go on site of BSE/CSE/NSE on which trade in specific case has took place.

B. Search for historic price movement curve and data vis-à-vis BSE/CSE/NSE for specific period. This bell shape curve in contrast with normal movement of BSE/CSE/NSE is a great indicator of bogus LTCG.

C. Download the financial results of company for year under consideration last few years.

D. Check data of day to day trade in that period. This data also have details of daily volume, which helps in proving that upward & downward movement in scrip is based on very thin volume, many a times, even single trade per day. This data can also be get from website like moneycontrol.com, and other financial trekking website.

E. If assessee has done any purchase or sale offline, what was price of the shares on that day.

F. Search in important announcement and note whether any such announcement is there in these websites.

G. Search for shareholding pattern, list of promoters, persons holding more than 1% shares, list of holding 5% shareholding etc.

H. Check for any history of blocking from trade by SEBI/BSE/NSE.

I. Most of these information in cases where information from wing is received or cases are selected on basis of ITD information or AIMS information, is already given in report in soft copy.

J. If website of listed company is available most of these information can also be get from there.

5.3 Information to be collected from assessee:

A. Copy of Demat account.

B. History of assessee in share transaction in earlier years.

C. In case of LTCL/STCL check about crystallization of extra ordinary income and try to match the same with purchase of shares resulted in LTCL/STCL.

D. Normal business of assessee, or family, firm/company in which assessee is major stock holders to trace the source of unaccounted cash in case of LTCG or use of accounted cash generated from LTCL/STCL.

E. Statement of assessee which can be taken at this stage too, by pointing out his in-efficiency for dealing in shares, and questioning his wisdom about investment in penny stocks, as companies are devoid of any financial worth.

F. Source of purported initial investment shown, whether in cash or cheque, and date of transfer of money from bank account of assessee. This leg is important in ascertaining that whether assessee has done any back dating, that is typical case when purchases are shown offline.

5.4 Information to be gathered from other sources:

A. Copy of contract notes, how the order was placed, trading account ledgers for all share transaction from broker of assessee.

B. Copy of Demat account, and documents given for KYC, Copy of contract notes, trading account ledgers for Demat account holder. For example sample letter is attached as Annexure-A to this SOP.

C. If shares has not been purchased by assessee online, and dematerialized lateron, ask information from Demat authority about documents on basis of which shares had been dematerialized. For example sample letter is attached as Annexure-B to this SOP.

D. Asking information from stock exchange BSE/NSE about all the trades done of specific scrips, for all purchase/sell including broker detail, purchase and sale party. For example sample letter is attached as Annexure-C to this SOP. These details are extremely important.

E. Checking for any punitive actions on any of such brokers by SEBI by checking SEBI website and google with their names by putting name of brokers/party and action by SEBI.

F. Check the data available in form of various reports from various investigation wings about brokers/and parties involved in trading, in this regard Kolkata investigatioin wing had already given summaried data with hyperlink to various statements.

G. Check from data available that whether the exit providers (bogus entity who purchases shares when sold by assessee) statement is available in database provided by wing.

H. Ask the details of KYC submitted and result of any background check done by broker, details of bank accounts, how the transactions has been ordered in respect of by purchase/seller parties as recd from stock exchange in reply to D from their brokers again recd in reply to D.

I. If shares had been purchased by preferential allotment of shares/or by merger, it is better to get the details of all preferential allotments, same is available at moneycontrol.com & BSE website, or Roc website, and trying analyse the trend of all such allotee, as all of these persons are beneficiary for bogus LTCG, an analysis of sale by all these parties in respect of gain from data recd in reply to D, along with all exit providers, is an excellent way to prove that entire thing is just a scam. Similarly, where shares issued to assessee of a pvt ltd company, which get merged with that listed company, it is better to get details of all persons whom shares have been issued by merged company on the same date as to the assessee, and then collate the same as in case of preferential allotment. For these purpose, information may be collected either from those parties, ROC, or even from bank statement of that party.

J. A backward probe in bank account of entities by asking information from banks at other end of assessee’s purchase and sale to reveal either cash deposit/cash withdrawal, detail regarding which is recd from brokers of those parties (as mentioned in H). For this purpose, it is better to either go personally in bank or through ITI, as many a times many layers accounts are maintained in same bank. For this purpose sample letter is attached as Annexure-D. while writing letters to bank, AO should refrain to write letters to original branch, as same wd not be in surat, writing letters to any branch, special regional branch in Surat should be suffice as all bank accounts are centralized as of now. This part is extremely important reaching to cash through layers is nearly proving cash beyond doubt.

K. Collecting information from assessing officers in respect of all entities recd as reply to D and all layers as found in

J. for this purpose, ITR may also be get from Investigation wing, as they have password where they can see return all India basis.

L. In case needed, commission may be issued to investigation wing to get the verification of parties entities and broker both involved in trade of that scrip (as recd in reply of D) if same is not already available, by giving the outline of case and investigation done so far.

M. Send the information collected so far to SEBI asking for details of any probe against scrip promoters/brokers/entities and if not done so, same may be requested to initiated in view of all the facts. In this letter, bell shaped curve, low volume and limited entities during price rise/fall, huge increase devoid of financial strength, bogus entities, not following of KYC norms and background check by brokers should be given.

5.5 Collate all the information and summoning the Assessee:

On the basis of above information, which broadly can be collated in five category Assessee must be issued summon second time (first time done as given in 5.3) section 131 of I.T.Act, a detailed statements should be recorded including:

wherein his knowledge about share market in general,

his knowledge about scrip specific

why and how investment was made.

How brokers were instructed

How well he knows the broker, its office, its employees

How his decision to purchase shares of scrip specific is devoid of financial wisdom,

Statements of entities specific if any.

Lying all the facts before him, which proves that transaction is not normal.

If one statement as given in para 5.3 are already been done, question already covered may be left and only he be affirmed on earlier statement.

5.6 Providing detailed showcause to assessee giving all the facts as a matter of natural justice with sufficient opportunity to reply. This showcause should include all the matters given in para 5.1

5.7 Drafting of final order after considering reply of assessee and facts gathered. Which should inter alia include:

i. Financial strength of scrip & price & volume trend, and other information from BSE website.

ii. Data regarding all players involved in movement of scrip, from stock exchange.

iii. Statements of exit providers and broker.

iv. History of SEBI action from internet & SEBI.

v. Backward probe in bank accounts of exit provider to find the cash trail.

(It is also important to mention that most information related to first four points is given by investigation wing in CD format, in the folders named as Invesigation report, LTCG Database, LTCG Trade ledgers, and SEBI orders, please check and analyse the same before calling from respective authorities.)

6. It is being clarified the above guidelines are not exhaustive or exclusive; the AO may delve deeper and also investigate from any other angle which the A.O. any consider necessary and appropriate.

Annexure-A

Office of the Income Tax Officer-

Pin Ph.

F. No. ITO/Ward-3(4)/133(6)/2015-16/ Date:

To,

The Manager/Authorised Signatory

Sir,

Subject: Information u/s 133(6) of IT Act 1961 in the case of

,

DP ID 12020600.

Please refer to the subject cited above.

In this regard, you are required to furnish the following details in respect of:-

1. Copy of his account opening forms (for both Demat and trading a/c) with your company along with KYC documents.

2. Copy of his trading account ledger in your books since opening to 31/03/2014

3. Copy of his Demat account statement since opening till 31/03/2014

4. Copy of contract notes (both sale and purchase) since opening of account till 31/03/2014

You are requested to furnish the required information by 12/08/2015 (statements should be duly certified). Soft copies of these documents/statements may be mailed to @incometax.gov.in Please note that this information is required u/s 133(6) of Income Tax Act 1961 and in case of non compliance penalty of ` 100/- for each day of default may be levied u/s 272A (2) (c).

Annexure-B

Office of the Income Tax Officer-Ward

Pin, Ph.

F. No. ITO/Ward-3(4)-/133(6)/2015-16/ Date: 05/11/2015

To,

The Director

Sir,

Subject: Information u/s 133(6) of IT Act 1961 in the case of Sh.

Demat No. 000

Please refer to the subject cited above.

In this regard, you are required to furnish the following details in respect of Sh.-

5. Copy of the share certificates/documents on the strength of which 2,00,000 shares of M/s Infra Ltd. were dematerialised and credited to his a/c on 27/01/2012.

You are requested to furnish the required information by 16/11/2015. Soft copies of these documents/statements may be mailed to @incometax.gov.in Please note that this information is required u/s 133(6) of Income Tax Act 1961 and in case of non compliance penalty of ` 100/- for each day of default may be levied u/s 272A (2) (c).

Annexure-C

Office of the Income Tax Officer-

Ph. @incometax.gov.in

F. No. ITO/Ward-3(4)-/2015-16/Date: 01/01/2016

To,

The Principal Officer/Director

Sir,

Subject: Notice u/s 133(6) of the Income Tax Act-1961- Regarding.

Kindly refer to the subject cited above.

2. In this regard it is stated that during the course of assessment proceedings in a case, this office requires following date wiseinformation in respect of trades made in the scrip ofM/s Kyra Landscapes Ltd. (security Id ABC, ISIN INE094M010):

2.1 List of DP/RTA/AP/Brokers who were involved in sale/purchase of this scrip from 17/06/2010 to 30/11/2011.

2.2 List of DP/RTA/AP/Brokers who were involved in sale/purchase of this scrip from 01/12/2011 to 29/10/2012.

2.3 Name, quantity bought/sold and other details (as available) of the persons who bought and sold this scrip during 17/06/2010 to 30/11/2011.

2.4 Name, quantity bought/sold and other details (as available) of the persons who bought and sold this scrip during 01/12/2011 to 29/10/2012.

3. Please also note that this information is required u/s 133(6) of Income Tax Act 1961 and in case of non-compliance penalty of ` 100/- for each day of default may be levied u/s 272A (2) (c). You are requested to send this information to the undersigned by 15th of January, 2016. Soft copies of the statements may be mailed as well.

For any clarification, please feel free to contact the undersigned on the numbers/email mentioned above.

Annexure-D

Office of the

No. Dated:

To

Name & Address of the Bank

SUMMONS UNDER SECTION 131 OF THE INCOME-TAX ACT, 1961

Whereas your attendance is required in connection with the proceedings under the Income-tax Act, 1961 in the case of ___________________, you are hereby required personally to attend my office at Room No.___, Aayakar Bhavan, on _______________ at _______ to give evidence and/or to produce personally the books of account or other documents specified hereunder and not to depart until you receive my permission to do so.

*(i) Copy of account opening form from the Bank account (to be asked only if letter is to investor’s Bank)

(ii) Copy of the instrument (cheque, DD, RTGS slip, NEIT instruction) both sides for the identified transaction, same has been highlighted in the Bank A/c. placed as annexure.

(iii) Name, address, Bank A/c. No., Bank details of the person from whom the transaction has been made.

(iv) If the transferor is also having account with your Bank, please submit –

(a) copy of account opening form along with the documents submitted for the same.

(b) copy of Bank statement for entire F.Y.2012-13.

(c) narration of all entries 10 days before and 10 days after the transaction date in names and addresses of the transferor and transferees and their Bank account details.

(v) Please also give details of all bank accounts who are linked with same Mobile No. and email id as provided by these persons.

(vi) If any of transferor and transferee mentioned in (iv)(c) has Bank A/c. in your Bank, then all details asked in (iv) &

(v) in respect of same and soon.

2. Without prejudice to the provisions of any other law for the time being in force, if you intentionally omit to so attend and given evidence or to produce the books of accounts and / or documents a penalty for a sum, which shall be to the extent of Rs. 10,000/- Rupees ten thousand) for each such default or failure shall be imposed upon you under section 272A(1)(C) of the Income-tax Act, 1961.

Name of the Officer