The CBDT has issued Circular No. 24/2017 dated 25th July 2017 in which it has provided clarifications on computation of book profit for the purposes of levy of Minimum Alternate Tax (MAT) under section 115JB of the Income-tax Act, 1961 for Indian Accounting Standards (Ind AS) compliant companies.

Government of India

Ministry of Finance

Department of Revenue

Central Board of Direct TaxesPRESS RELEASE

New Delhi, 25th July, 2017.Issues arising from the implementation of Minimum Alternate Tax (MAT) provisions relating to Indian Accounting Standards (Ind AS) compliant companies.

Finance Act, 2017 amended the provisions of section 115JB of the Incometax Act,1961(‘the Act’) so as to provide the framework for computation of book profit for the purposes of levying Minimum Alternate Tax (MAT) in case of Indian Accounting Standards (Ind AS) compliant companies in the year of adoption and thereafter. This framework was specified on the basis of the recommendations of the MAT-Ind AS Committee (‘the Committee’) constituted for this purpose.

Subsequently, representations have been received from various stakeholders regarding certain issues arising from the implementation of provisions of amended section 115JB of the act. These representations were forwarded to the Committee for examination. After detailed examination of implementation issues raised by the stakeholders, the Committee vide report dated 17th June, 2017 has recommended certain amendment to the provisions of section 115JB of the Act with effect from 1st April,2017 (i.e. A.Y.2017-18) which is the date of coming into effect of the amendments made in section 115JB of the Act by the Finance Act, 2017.

The recommendations of the Committee regarding issuance of circular in the form of FAQs have been accepted by the Government and circular in the form of FAQs has been issued vide No 24/2017 dated 25.07.2017.

Further, in order to have wider consultation in response of Committee’s recommendations regarding amendment to the provisions of section 115JB of the Act w.e.f. 1st April, 2017, the relevant part of the Committee’s Report has been uploaded on the department website: www.incometaxindia.gov.in. The stakeholders are requested to send the comments/ suggestions on E-mail ID dirtpl2@nic.in latest by 11th August, 2017.

(Surabhi Ahluwalia)

Commissioner of Income Tax

(Media & Technical Policy)

Official Spokesperson, CBDT.

Circular Number 24/2017

F. No 133/23/2015-TPL

Government of India

Ministry of Finance

Department of Revenue

Central Board of Direct Taxes

(TPL Division)

****

Dated 25th July, 2017Subject: Clarifications on computation of book profit for the purposes of levy of Minimum Alternate Tax (MAT) under section 115JB of the Income-tax Act, 1961 for Indian Accounting Standards (Ind AS) compliant companies.

Central Government notified the Indian Accounting Standards (Ind AS) which are converged with International Financial Reporting Standards (IFRS) vide Companies (Indian Accounting Standards) Rules, 2015. Consequently, the Finance Act, 2017, has amended the provisions of section 115JB of the Income-tax Act, 1961 (‘the Act’) for Ind AS compliant companies w.e.f. 1st day of April, 2017 (A.Y. 2017-18).

The Central Board of Direct Taxes (‘the Board ‘) has received representations from various stakeholders seeking clarifications on certain issues arising therefrom. The matter was referred to an expert committee. The Committee after duly considering the representations from stakeholders has recommended issuance of clarifications by way of FAQs for these issues.

The matter has been considered by the Board and the following clarifications are issued.

Question 1: The profit for the period may include Marked to market (MTM) gains/ losses on account of fair value adjustments on various financial instruments recognised through profit or loss (FVTPL). A situation may arise where the losses on account of fair value adjustments could be added back in view of clause (i) of Explanation 1 to section 115JB (2) of the Act. Whether the losses on such instruments require any adjustment for computing book profits for the purposes of MAT?

Answer: Since MTM gains recognised through profit or loss on FVTPL classified financial instruments are included in book profits for MAT computation, it is clarified that MTM losses on such instruments recognised through profit or loss shall not require any adjustments as provided under clause (i) of Explanation 1 to section 115JB(2) of the Act. However, in case of provision for diminution/ impairment in value of assets other than FVTPL financial instruments, the existing adjustment of clause (i) of Explanation 1 to section 115JB (2) of the Act shall apply.

It is further clarified that for financial instruments where gains and losses are recognised through Other Comprehensive income (OCI), the amended provisions of MAT shall continue to apply.

Question 2: For the purposes of section 115JB of the Act, what shall be the starting point for computing Book profits for Ind AS compliant companies? Whether Profit before other comprehensive income [Item number XIII in Part 2 (Statement of Profit and Loss) of Division II of Schedule III to the Companies Act 2013] or Total Comprehensive Income(including other comprehensive income)[Item number XV in Part 2 (Statement of Profit and Loss) of Division II of Schedule III to the Companies Act 2013] shall be the starting point?

Answer: Starting point for computing Book profits for Ind AS compliant companies shall be Profit before other comprehensive income [Item number XIII in Part 2 (Statement of Profit and Loss) of Division II of Schedule III to the Companies Act 2013].

Question 3: As per Explanation to Section 115 JB (2C) of the Act, the convergence date is defined as the first day of the first Indian Accounting standards reporting period as defined in Ind AS 101. The Memorandum explaining the provisions of the Finance Bill 2017 mentions that the adjustment as on the last day of the comparative period is to be considered. It may be clarified as to what would be the appropriate manner for computation of transition amount on convergence date, 1st April i.e. at the start of the day or at the end of the day?

Answer: In the first year of adoption of Ind AS, the companies would prepare Ind AS financial statement for reporting year with a comparative financial statement for immediately preceding year. As per Ind AS 101, a company would make all Ind AS adjustments on the opening date of the comparative financial year. The entity is also required to present an equity reconciliation between previous Indian GAAP and Ind AS amounts, both on the opening date of preceding year as well as on the closing date of the preceding year. The amounts as on start of the opening date of the first year of adoption should be considered for the purposes of computation of transition amount.

For example, companies which adopt Ind AS with effect from 1st day of April 2016 are required to prepare their financial statements for the year 2016-17 as per requirements of Ind AS. Such companies are also required to prepare an opening balance sheet as of 1st day of April 2015 and restate the financial statements for the comparative period 2015-16. In such a case, the first time adoption adjustments as of 31st day of March 2016 should be considered [i.e. the start of business on 1st day of April 2016 (or, equivalently, close of business on 31st day of March 2016)] for computation of MAT liability for previous year 2016-17 (Assessment year 2017-18) and thereafter.

Question 4: As per Indian GAAP, proposed dividend was required to be recognized in the financial statements for the year for which it pertained to even though these were declared in the subsequent year. Section 115JB of the Act already provides for adjustments for dividend for computation of book profit. As per Ind AS, the amount of proposed dividend (including dividend distribution taxes) is required to be recognized in the year in which it has been declared rather than the year for which it pertains to. Accordingly, on transition to Ind AS, the amount of proposed dividend for FY 2015-16 which was recognized in profit and loss account in FY 2015-16 is required to be reversed and credited to Retained Earnings. For the computation of MAT, whether these balances would form part of the transition amount and thus be adjusted over a period of 5 years?

Answer: Adjustment of proposed dividend (including dividend distribution taxes) shall not form part of the transition amount.

Question 5: Under Ind AS, adjustments on the transition date may have a corresponding impact on deferred taxes. Should the deferred taxes on such amounts be considered for the purpose of transition amount?

Answer: Any deferred taxes adjustments recorded on the transition date shall be ignored for the purpose of computing Transition Amount.

Question 6: As mentioned in Question No.1, clause (i) of Explanation 1 to Section 115JB(2) of the Act provides for adjustments for computation of book profit for the amount or amounts set aside as provision for diminution in the value of any asset. Convergence date adjustments may include adjustment for Provision for Bad and Doubtful Debts (Expected Credit Loss adjustment) at the time of transition. Whether these adjustments would form part of the transition amount referred to in section 115JB(2C) of the Act?

Answer: Adjustments relating to provision for diminution in the value of any assets other than the ones mentioned in Question Number 1 above, shall not be considered for the purpose of computation of the Transition Amount. Therefore, adjustments relating to provision for doubtful debts shall not be considered for the purpose of computation of the transition amount.

Question 7: Under Section 115 JB of the Act, transition amount has been defined as the amount or the aggregate of the amounts adjusted in the ‘Other Equity’ (excluding capital reserve and securities premium reserve) on the convergence date. Whether changes in share application money on reclassification to ‘Other Equity’ would form part of the Transition Amount?

Answer: Share application money pending allotment which is reclassified to Other Equity on transition date shall not be considered for the purpose of computing Transition Amount.

Question 8: Under Ind AS, Investments in preference share is considered to be a liability and the corresponding dividend expense is debited to Profit and loss account as interest cost. Should such interest expenses on preference shares be deducted for the purpose of MAT computation?

Answer: For the purpose of computation of MAT, profit/Transition Amount shall be increased by dividend/interest on preference share (including dividend distribution taxes) whether presented as dividend or interest.

Question 9: How do we account for items such as equity component, if any, of financial instruments like Non-Convertible debentures (NCDs), Interest free loan etc. included in other equity as per Ind AS for the computation of transition amount under MAT?

Answer: Items such as equity component of financial instruments like NCD’s, Interest free loan etc. would be included in the Transition Amount.

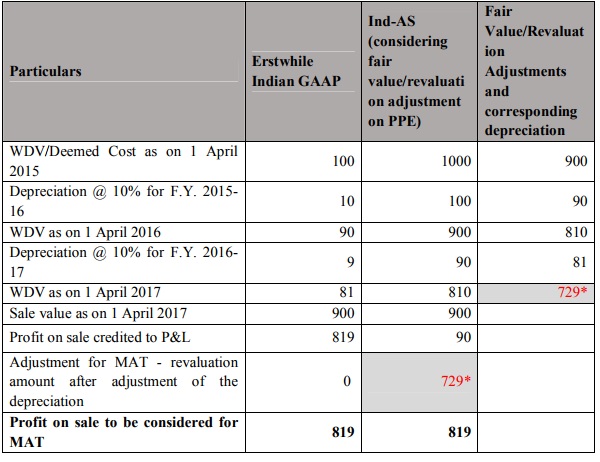

Question 10: Where revaluation/ fair value adjustments have been made to items of Property, Plant & Equipment (PPE) under Ind AS, as per section 115JB of the Act, the book profit of the previous year in which the items of PPE are retired, disposed or realised shall be increased or decreased, as the case may be, by the revaluation amount relatable to such items of PPE. Whether the revaluation amount to be considered for adjustment should be the gross amount of the revaluation or the amount after adjustment of the depreciation on the revaluation amount?

Answer: The book profit of the previous year in which the items of PPE are retired, disposed, realised or otherwise transferred shall be increased or decreased, as the case may be, by the revaluation amount after adjustment of the depreciation on the revaluation amount relatable to such asset. This has been explained by an illustration as under:

Question 11: How should adjustments for service concession arrangements be treated for the purpose of computation of book profit under MAT?

Answer: Adjustments on account of Service Concession arrangements would be included in the Transition Amount and also on an ongoing basis.

Question 12: Existing clause (iii) of explanation to section 115JB(2) of the Act provides for deduction of lower of the amount of loss brought forward or unabsorbed depreciation as per books of account for computation of book profits. In case where, on adjustment of transition amount, the losses as per books of account gets wiped off, whether deduction for the said amount would be available for assessment year 2017-2018 onwards?

Answer: For assessment year 2017-2018, the deduction of lower of depreciation or losses shall be allowed based on the position as on 31 March 2016. For the subsequent periods, the position as per books of account drawn as per Ind AS shall be considered for computing lower of loss brought forward or unabsorbed depreciation.

Question 13: How Capital Reserves or Securities Premium existing as per old Indian GAAP reclassified to Retained Earnings/ Other Reserves on Convergence date be treated for MAT purpose.

Answer: The Capital Reserves or Securities Premium existing as on the convergence date as per the erstwhile Indian GAAP which are reclassified to Retained Earnings/ Other Reserves under Ind AS and vice versa, shall not be considered for the purposes of Transition Amount.

It is further clarified, that even after such reclassifications, the amount of revaluation reserve shall continue to be considered as revaluation reserve for the purposes of computation of book profit and shall also include transfer to any other reserves by whatever name called or capitalised.

Question 14: Companies which follow accounting year other than March, 2017 ending for Companies Act purposes and are required to transition to Ind AS will have to prepare financial statements for MAT purposes for FY 2016-17 partly under Indian GAAP and partly under Ind AS. How should such companies compute MAT on transition to Ind AS?

Answer: In view of second proviso to section 115JB (2) of the Act, companies will be required to follow Indian GAAP for the pre-convergence period and Ind AS for the balance period.

For example, a Company following December ending will be required to prepare, accounts for MAT purposes under Indian GAAP for 9 months upto December 2016 and under Ind AS for 3 months thereafter. The transition amount will be calculated with reference to 1st January, 2017.

(Abhishek Gautam)

Under Secretary to the Government of India

The email has been made mendetory in form 15G & 15H in

SBI. But most of the customers are not literate for it

So it may be considered before complition of April.